Tax basics and qualified distributions

Roth IRAs are funded with after-tax dollars; qualified distributions are generally income-tax-free, subject to ordering rules and eligibility criteria. IULs grow on a tax-deferred basis, and policy loans or withdrawals have different tax consequences depending on basis, policy funding, and whether the policy is a Modified Endowment Contract (MEC). Neither substitute for professional tax guidance—use the provided Roth vs IUL breakeven calculator to model tax outcomes under different assumptions.

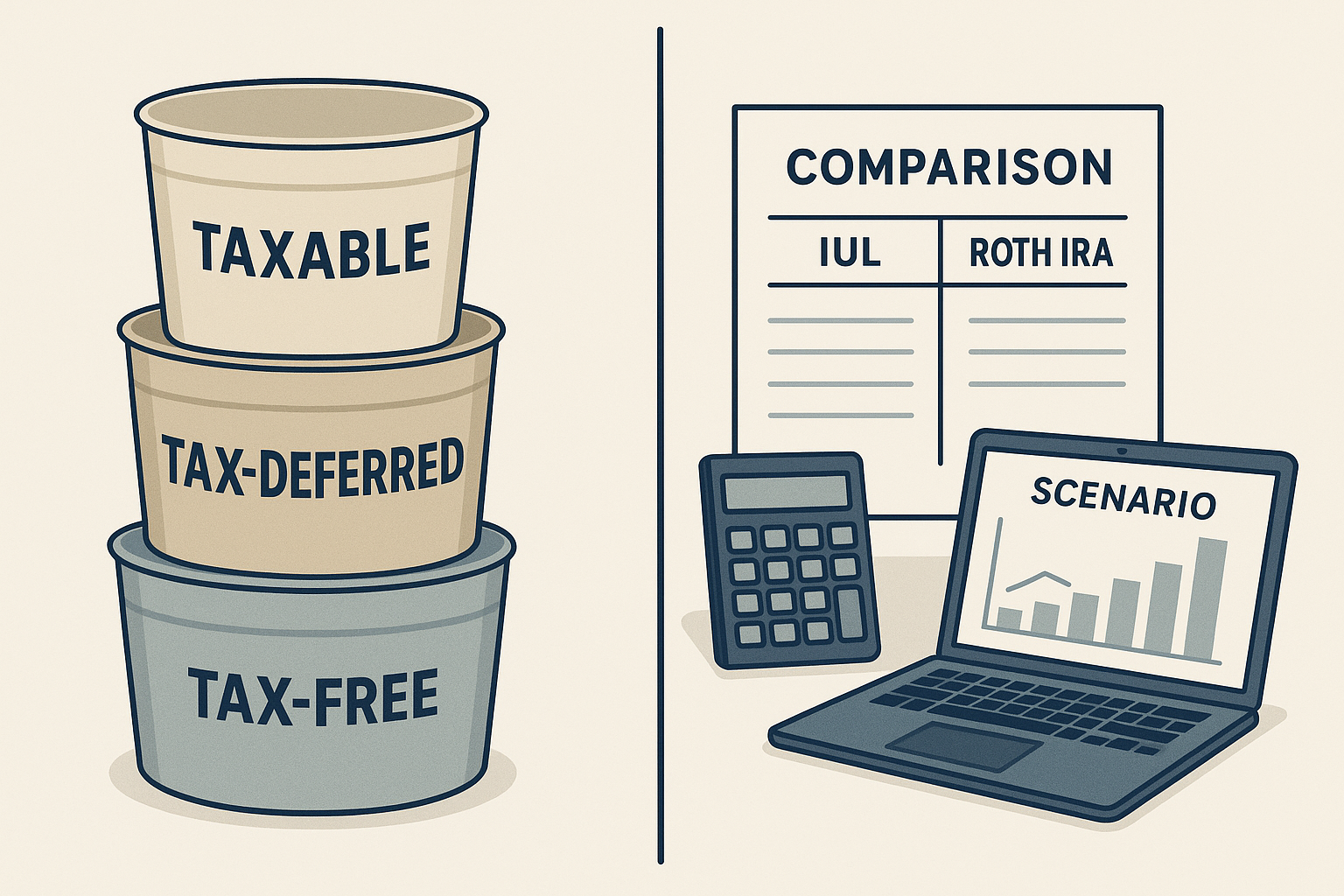

Liquidity, access, and sequencing

Roth IRAs generally allow penalty-free qualified distributions for account holders meeting age and holding period requirements, while IULs offer cash-value access via loans and withdrawals that may avoid immediate taxation but can affect policy performance and death benefit. Compare restrictions, surrender charges, and how each product fits into a withdrawal sequence (taxable first, tax-deferred next, tax-free last) under different scenarios. Link to the side-by-side scenario tool to model income sequences.

Costs, guarantees, and long-term growth

IULs can provide a death benefit and protection from downside via floors, but fees, cost of insurance, and cap/participation features can limit upside. Roth IRAs invest directly in market instruments—returns are subject to market risk but without embedded insurance costs. Use comparison tables to test net returns after fees, and a calculator to project break-even horizons where an IUL's additional costs might be offset by tax-sheltering or legacy value.

Practical decision framework

No single option is universally 'better.' Consider: 1) primary objective (tax-free income vs legacy vs guaranteed income), 2) time horizon, 3) tolerance for fees and complexity, 4) ability to fund Roth contributions or conversions, and 5) desire for downside protection. Run side-by-side scenarios and discuss findings with a qualified advisor before acting. CTA: Try our side-by-side scenario tool or schedule an advisor consult to test real-world inputs.

Frequently Asked Questions

Can an IUL provide tax-free retirement income like a Roth IRA?

IULs can offer tax-deferred growth and access to cash value through policy loans or withdrawals, which in some circumstances may be accessed without immediate income taxation. A Roth IRA's qualified distributions are generally income-tax-free for eligible accounts. The tax outcomes for IULs depend on policy design, cost of insurance, loan usage, and whether the policy becomes a Modified Endowment Contract. Use modeling tools and consult a tax professional for personalized outcomes.

Is a fixed indexed annuity a safer alternative to an IUL?

Fixed indexed annuities and IULs both use index-linked crediting with downside floors, but they serve different purposes. FIAs are typically designed for guaranteed accumulation or lifetime income and may limit liquidity due to surrender periods or annuitization. IULs provide life insurance protection plus cash value access that can be flexible but carries insurance costs. Safety depends on product features, carrier strength, and how the product is used in a plan.

Should I use taxable accounts before tapping an IUL or Roth?

Many planners model withdrawal sequencing—often using taxable accounts first, then tax-deferred accounts, and preserving Roth assets—but the optimal sequence depends on individual tax rates, liquidity needs, and market conditions. An IUL may change sequencing because loans or withdrawals can provide supplemental liquidity. Run side-by-side scenarios with your actual inputs and consult a qualified advisor for tailored guidance.

Related Articles in This Series

Plan Your Retirement Income With Confidence

If this topic raised questions about retirement income, taxes, market risk, or long-term planning, the next step is to review a simple educational guide and prepare for a strategy conversation.

Download the free guide: Comparing IULs with Roth IRAs, Fixed Indexed Annuities, and Taxable Accounts for Retirement Income