In This Series

Key Takeaways

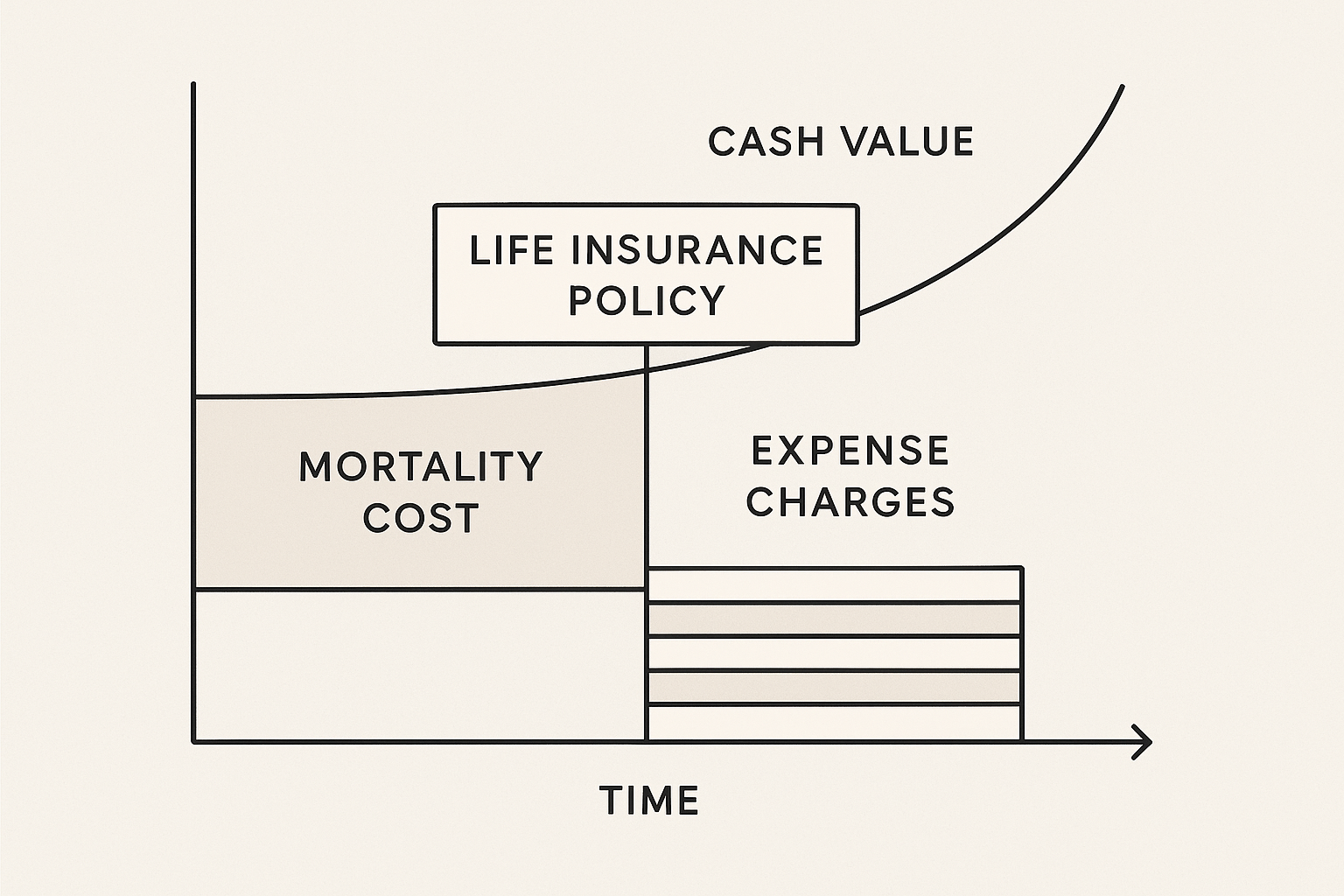

- Mortality costs and other policy charges typically increase with age and can significantly reduce cash value growth if funding is insufficient.

- Modeling should include sensitivity to rising cost-of-insurance assumptions and consider premium top-up scenarios to absorb higher charges.

- Longevity planning requires contingency actions—such as conservative withdrawal pacing, premium cushion, and regular policy reviews—to reduce the risk of policy depletion.

Angle: Offer clear analysis of charge structures and operational approaches to mitigate the impact of rising mortality costs while preserving income flexibility.

Understanding the Components of Policy Charges

IUL policies include several types of charges that reduce cash value accumulation: mortality and expense charges, administrative fees, load charges on premiums, and fees tied to specific riders. Mortality charges reflect the insurer’s cost of providing the death benefit and typically rise as the insured ages. Other fees may be fixed or percentage-based and can vary across carriers and product generations. A thorough review of the illustration pages that show these charges, and how they apply under different funding scenarios, gives planners the insight needed to build robust funding strategies.

Modeling Cost Sensitivity and Funding Strategies

Because mortality charges tend to increase over time, running models that stress higher cost-of-insurance scenarios is essential. Planners should construct contingency funding paths that show the effect of premium top-ups at specific trigger points and estimate how much additional premium would be required to maintain policy performance under adverse cost trends. Conservative base-case assumptions and periodic re-evaluation reduce the chance that the policy will require abrupt corrective actions or lapse when the insured is older.

Longevity Risk and Contingency Planning

Longevity risk—outliving the policy’s capacity to support distributions—can be mitigated through cautious withdrawal rates, an explicit cash reserve, and a documented plan for interventions if projected cash value trajectories fall short. Maintaining a modest cushion in premium funding during accumulation, staging distributions to preserve core cash value, and scheduling regular check-ins are practical governance measures. These tactics, together with sensitivity modeling and trigger-based actions, equip advisors and pre-retirees to manage the uncertainty inherent in long retirement horizons.

Related Articles

- Implementing IUL Strategies for Retirement Income: Design, Risks, and Steps

- IUL Crediting Strategies: Caps, Participation Rates, and Index Choices

- Policy Loans and Withdrawals: Structuring Distributions from IULs

- 401k Retirement Income Strategy: How to Turn Savings Into a Reliable Paycheck

- 7 Retirement Risks That Could Derail Your Retirement Plan

Plan Your Retirement Income With Confidence

If this topic raised questions about retirement income, taxes, market risk, or long-term planning, the next step is to review a simple educational guide and prepare for a strategy conversation.

Download the free guide: Implementing IUL Strategies for Retirement Income: A Practical Guide for Advisors and Savvy Pre-Retirees