In This Series

In This Guide

Key Takeaways

- A breakeven analysis compares cumulative nominal benefit totals or present value equivalents for different claiming ages.

- Results depend heavily on assumed life expectancy and whether you discount future dollars to present value.

- Work-related factors, spousal benefits, and health costs can shift the breakeven age and should be included in household scenarios.

Angle: Walk readers through simple, reproducible calculations and clear examples so they can see when delaying benefits outpaces early claiming under realistic life-expectancy assumptions.

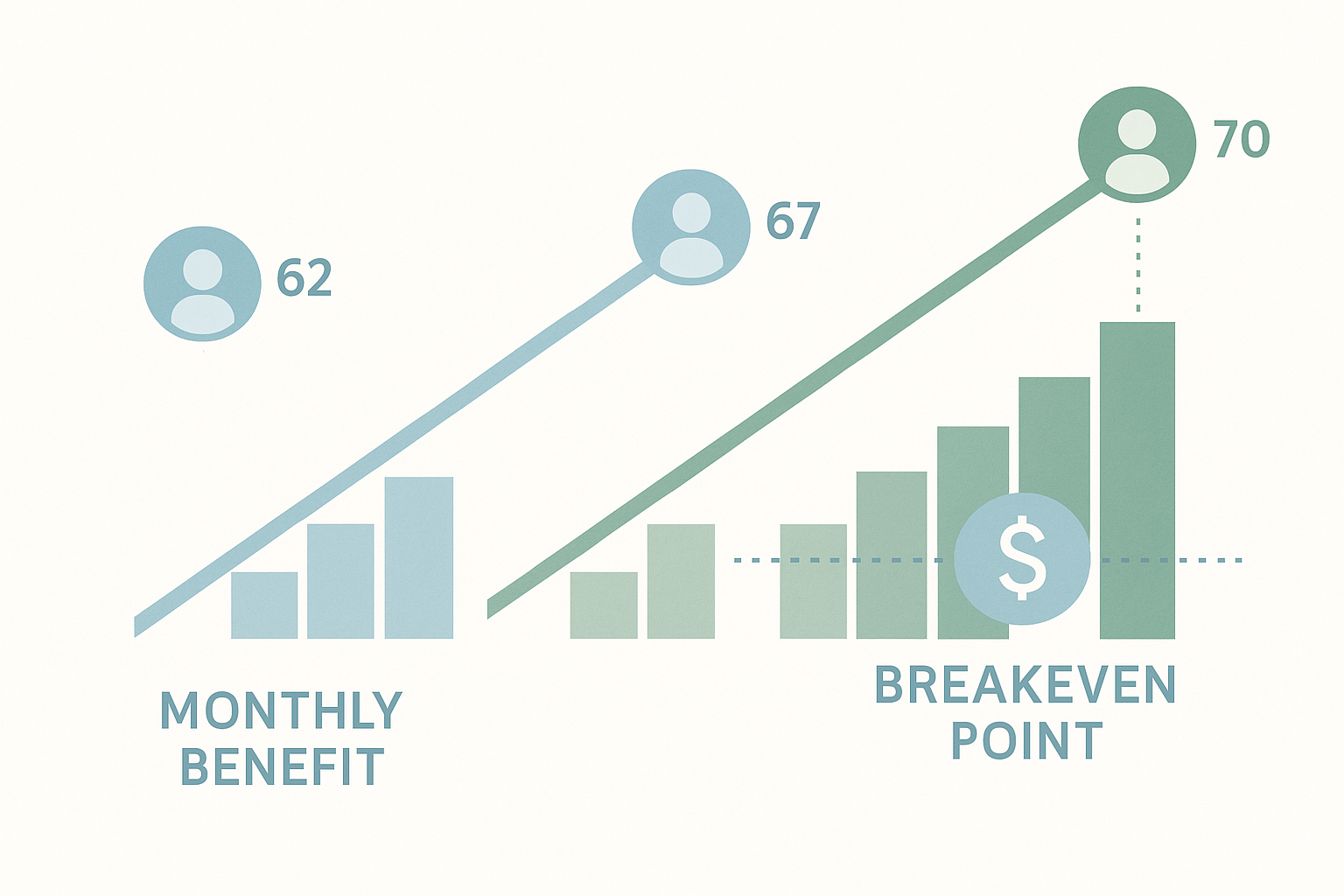

Setting Up the Calculation

Begin by collecting estimated monthly benefits at the ages you want to compare. Use the Social Security Administration’s online statement or a benefits calculator to obtain baseline numbers for claiming at 62, FRA (often 67), and 70. Decide whether you will compare nominal cumulative payments or compute present values using a discount rate. For nominal comparisons, simply add up the monthly checks year by year. For present-value comparisons, select a conservative discount rate to reflect alternative investment returns or the household’s time preference for money. Write down life-expectancy scenarios you want to test, such as median life expectancy, a longer horizon to account for family longevity, and a shorter horizon to reflect health concerns.

Worked Examples and Interpretation

Run at least three example scenarios. In the first, use a median life expectancy and add nominal payments by year for each claiming age to find the calendar year when delayed claiming pays more in total dollars. In the second, present-value both series using a modest discount rate to see how valuing future dollars changes the breakeven age. In the third, include a scenario where the higher earner delays to increase survivor protection, and compare household-level totals for different spouse combinations. Interpret results carefully: a late breakeven year suggests early claiming may be better for shorter lives or for households prioritizing present income, while a later-claiming advantage supports maximizing long-term protected income.

Common Pitfalls and Practical Tips

Avoid relying on a single scenario. Small changes in life-expectancy assumptions, the chosen discount rate, or inclusion of spousal benefits can flip the result. Remember to account for Medicare premiums and taxes on Social Security benefits since these affect net receipts. If you work while claiming, factor in possible temporary reductions under the earnings test and how they are recredited. Finally, document your assumptions and save calculations so you can revisit them if your financial or health outlook changes. The main article “When Should You Take Social Security? (62 vs 67 vs 70)” discusses how these calculations fit into broader retirement planning decisions.

Related Articles

- When Should You Take Social Security? (62 vs 67 vs 70) — How to Compare Your Options

- Spousal, Survivor, and Divorced Benefits Explained

- How Working While Claiming Affects Social Security and Medicare

- Implementing IUL Strategies for Retirement Income: Design, Risks, and Steps

- 7 Retirement Risks That Could Derail Your Retirement Plan

- 401k Retirement Income Strategy: How to Turn Savings Into a Reliable Paycheck

About the Author

John P. Sansaricq is a licensed insurance professional focused on retirement income planning, life insurance strategies, and educational resources for pre-retirees and retirees.

He helps individuals and families explore ways to protect savings, manage risk, and prepare for more informed retirement planning conversations.

Plan Your Retirement Income With Confidence

If this topic raised questions about retirement income, taxes, market risk, or long-term planning, the next step is to review a simple educational guide and prepare for a strategy conversation.

Download the free guide: When Should You Take Social Security? (62 vs 67 vs 70) — A Practical Guide