In This Series

In This Guide

Key Takeaways

- Claiming at 62 provides earlier cash flow but results in a permanently reduced monthly benefit compared with FRA.

- Claiming at full retirement age gives the unreduced benefit based on your earnings record; delaying to 70 increases monthly benefits through delayed credits.

- A breakeven analysis helps compare cumulative benefits under different claiming ages and should be tested against realistic life-expectancy and household scenarios.

- Spousal and survivor benefits, working while claiming, and Medicare timing materially affect the optimal claiming age for couples.

- Documenting assumptions and periodically revisiting the decision keeps your plan aligned with changing circumstances.

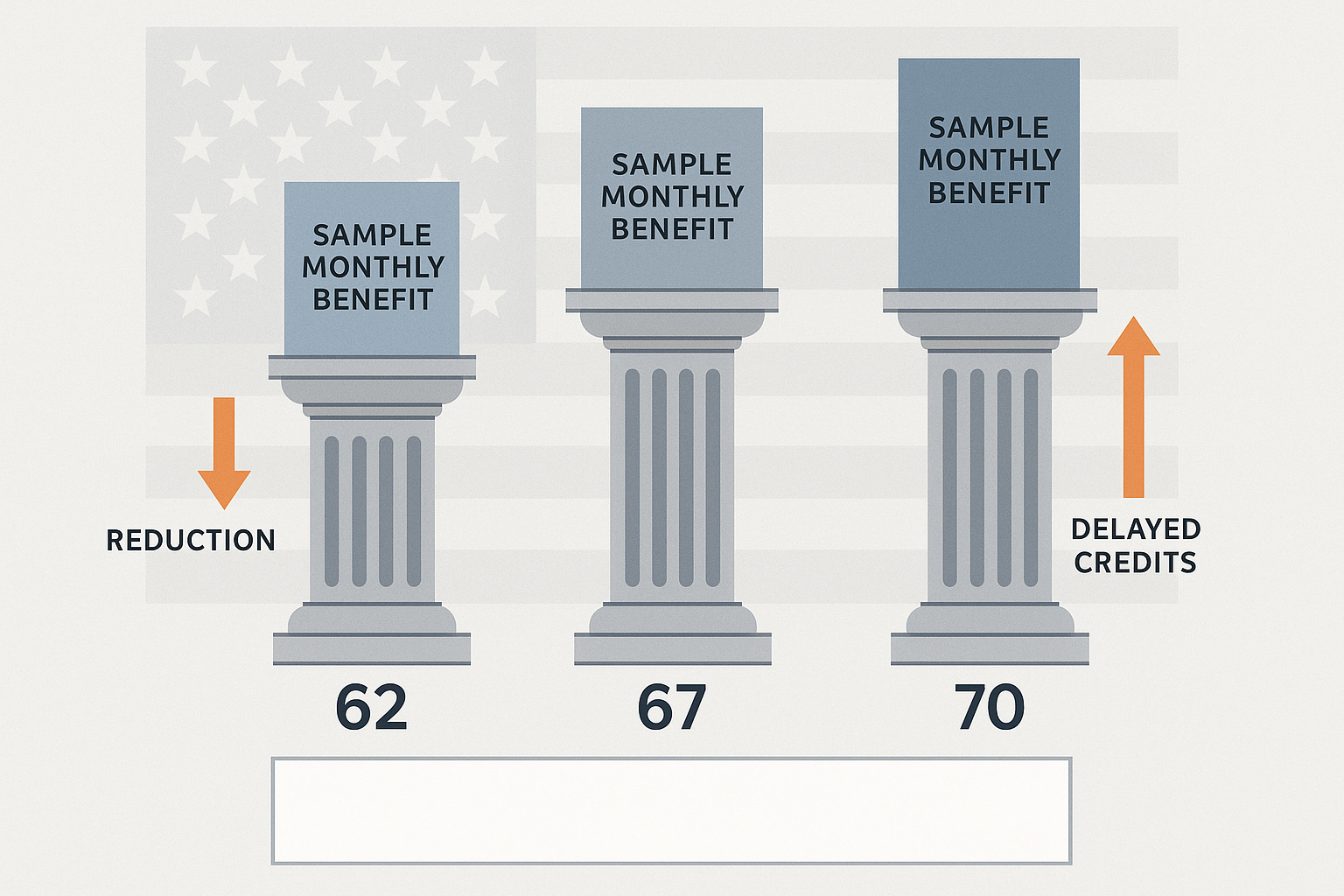

What Happens to Your Monthly Benefit at 62, 67, and 70

Monthly Social Security benefits depend on your age at claim and your earnings history. If your full retirement age is 67 and you claim at 62, your monthly benefit will be substantially lower than at FRA because the benefit is reduced for each month you claim early. Conversely, waiting past FRA up to age 70 increases your monthly benefit through delayed retirement credits at a roughly 8% annual rate for people with an FRA of 67, producing a roughly 24% larger benefit at 70 than at 67. These changes are permanent for that person’s benefit amount, so the monthly income trade-off between claiming early and delaying should be viewed in the context of cumulative lifetime receipts and household needs.

How to Do a Practical Breakeven Comparison

A breakeven comparison sums expected benefit payments under different claiming ages and identifies the year when the delayed larger payments surpass the smaller earlier ones. Start with estimated monthly benefits at each claiming age—SSA offers online estimates that can be used as starting numbers. Choose a life-expectancy scenario, such as age 82, 86, or 90, and add up benefits year by year under each claiming age. Although discounting future dollars is appropriate if you compare value today, many households simply want the calendar breakeven year to understand when delaying pays off in cumulative nominal dollars. The supporting article “How to Run a Social Security Breakeven Analysis” provides worked examples and a downloadable worksheet you can adapt to your situation.

Couples, Spouses, and Survivors: Coordination Matters

When two people fall under the same household roof, the claiming decision for each partner affects the household’s lifetime Social Security income. A higher earner who delays can increase the survivor benefit available to a spouse, which can be an important protection if one partner outlives the other. Spousal benefits may also provide a floor for a lower-earning spouse, and divorced-worker rules may apply in some situations. For these reasons, married couples often evaluate combinations of claiming ages rather than treating each person’s decision independently. The supporting article “Spousal, Survivor, and Divorced Benefits Explained” walks through common couple scenarios and how coordination can change the best timing for each spouse.

The Role of Work, Earnings Limits, and Medicare Timing

Working while claiming Social Security before full retirement age can temporarily reduce benefit payments if earnings exceed the annual earnings limit; however, those withheld benefits are not lost but typically recredited when you reach FRA. After FRA there is no earnings limit. Also, because Medicare eligibility normally begins at age 65, if you delay Social Security past that age you need to consider how health coverage and its cost will be managed until benefits begin. Taxes on Social Security benefits and potential premiums for Medicare Part B and Part D further interact with claiming decisions. The supporting article “How Working While Claiming Affects Social Security and Medicare” explains how the earnings test, Medicare enrollment, and tax thresholds commonly alter real-world outcomes.

Putting Numbers and Values Together for a Decision

Numbers alone don’t determine the right claiming age; values, risk tolerance, and household priorities do. For example, if your priority is maximizing protected lifetime income and you have other resources to cover early years, delaying may make sense. If you need dependable monthly cash flow immediately, an earlier claim is logical. Build a decision checklist: obtain SSA estimates, test several life-expectancy scenarios, include spousal and survivor effects, and factor in work, Medicare, and taxes. Write down your assumptions and revisit them if health, employment, or family status changes. Thinking through these elements with clear estimates can help families and retirees make a choice that aligns with both their finances and personal priorities.

Frequently Asked Questions

If I claim Social Security at 62, is my benefit permanently lower?

Yes. If you claim before your full retirement age, your monthly benefit is permanently reduced to reflect the longer period over which benefits are paid. The reduction amount depends on your full retirement age and how many months you claim early. These reductions affect the ongoing monthly check and the survivor benefit calculation.

Will delaying to age 70 always give me more lifetime benefits?

Not necessarily. Delaying increases your monthly benefit due to delayed retirement credits, but whether that produces greater lifetime benefits depends on life expectancy, household circumstances, and alternative uses for the income. A breakeven analysis under several life-expectancy scenarios clarifies when delaying yields higher cumulative benefits for you and your family.

How does working after claiming affect my Social Security checks?

If you claim before full retirement age and continue to work, Social Security applies an earnings test that can reduce your benefit payments temporarily if your earnings exceed the annual limit. Withheld amounts are typically recredited when you reach full retirement age and can increase later benefits. After full retirement age there is no earnings test.

Related Articles in This Series

- How to Run a Social Security Breakeven Analysis

- Spousal, Survivor, and Divorced Benefits Explained

- How Working While Claiming Affects Social Security and Medicare

- IULs vs Fixed Indexed Annuities for retirement income: How to Compare the Two

- 401k Retirement Income Strategy: How to Turn Savings Into a Reliable Paycheck

- The 401(k) Tax Trap Most Retirees Don’t See Coming — What It Is and How to Respond

About the Author

John P. Sansaricq is a licensed insurance professional focused on retirement income planning, life insurance strategies, and educational resources for pre-retirees and retirees.

He helps individuals and families explore ways to protect savings, manage risk, and prepare for more informed retirement planning conversations.

Plan Your Retirement Income With Confidence

If this topic raised questions about retirement income, taxes, market risk, or long-term planning, the next step is to review a simple educational guide and prepare for a strategy conversation.

Download the free guide: When Should You Take Social Security? (62 vs 67 vs 70) — A Practical Guide