Angle: Provide practical, data‑driven examples and a clear method for performing break‑even calculations, helpful for DIY planners and advisors alike.

The Mechanics of Delayed Retirement Credits

Explain how delayed credits increase benefits up to age 70, the typical percentage per year (educational description without advising), and how COLA interacts with delayed amounts. Provide a short numeric example showing the monthly increases from delaying at ages 66, 67, and 70.

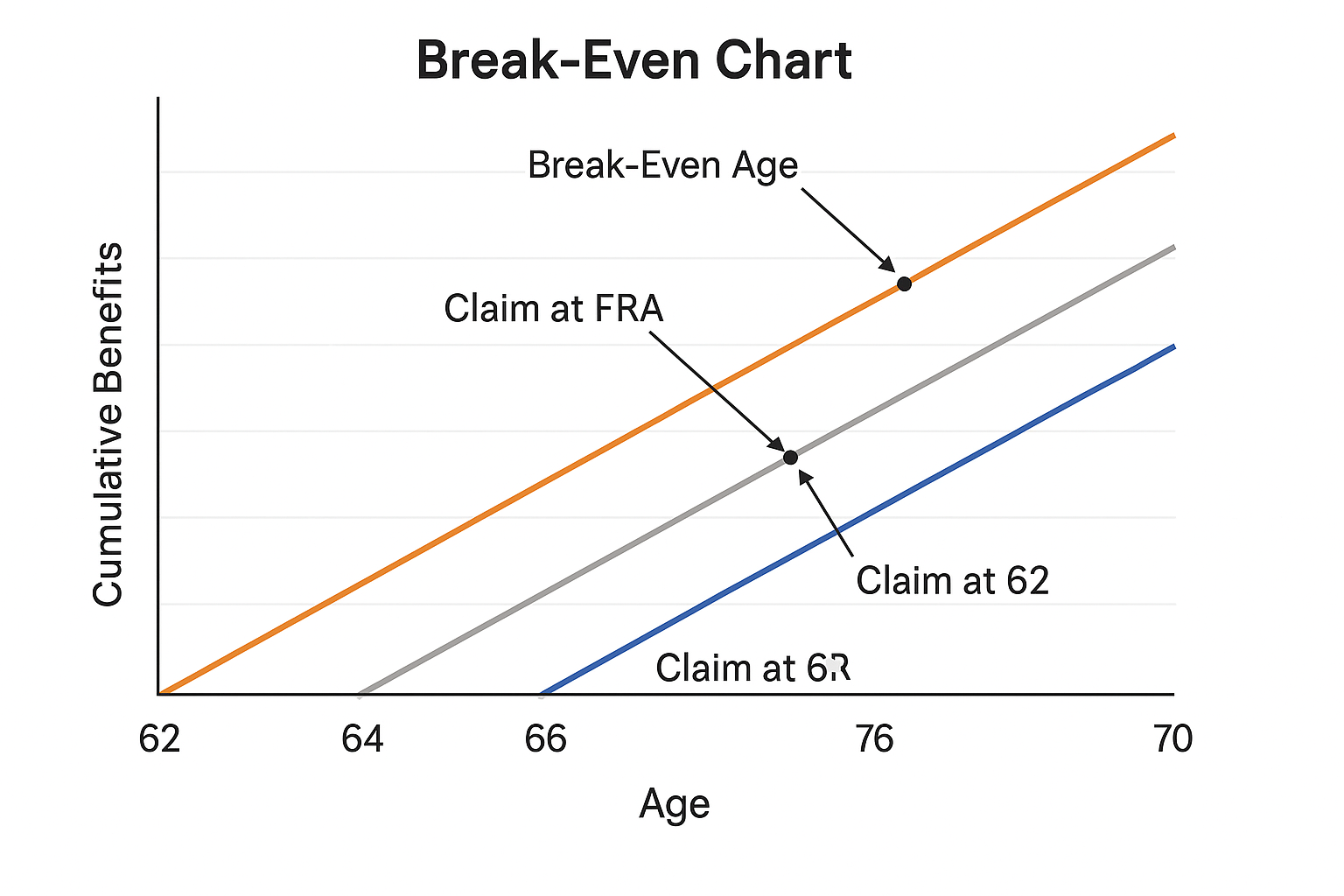

How to Run a Break‑even Analysis: Step‑by‑Step

Give a repeatable method: estimate monthly benefits at different claiming ages, calculate cumulative benefits year by year, plot or tabulate cumulative totals, and identify the age when the delayed claim surpasses the earlier claim (the break‑even age). Recommend running sensitivity checks for lifespan and discount rates.

Case Studies: When Delaying Helps and When It Doesn’t

Three case studies: (1) healthy high earner with strong family longevity — delaying favored; (2) single person with immediate income needs — early claiming may be appropriate; (3) couple with asymmetric earnings where survivor protection is critical — delaying the higher earner may be beneficial. Each study shows the break‑even age and discusses nonfinancial factors to consider.

Related Articles

Plan Your Retirement Income With Confidence

If this topic raised questions about retirement income, taxes, market risk, or long-term planning, the next step is to review a simple educational guide and prepare for a strategy conversation.

Download the free guide: How to Maximize Social Security: Timing, Spousal/Survivor Benefits, and Strategies