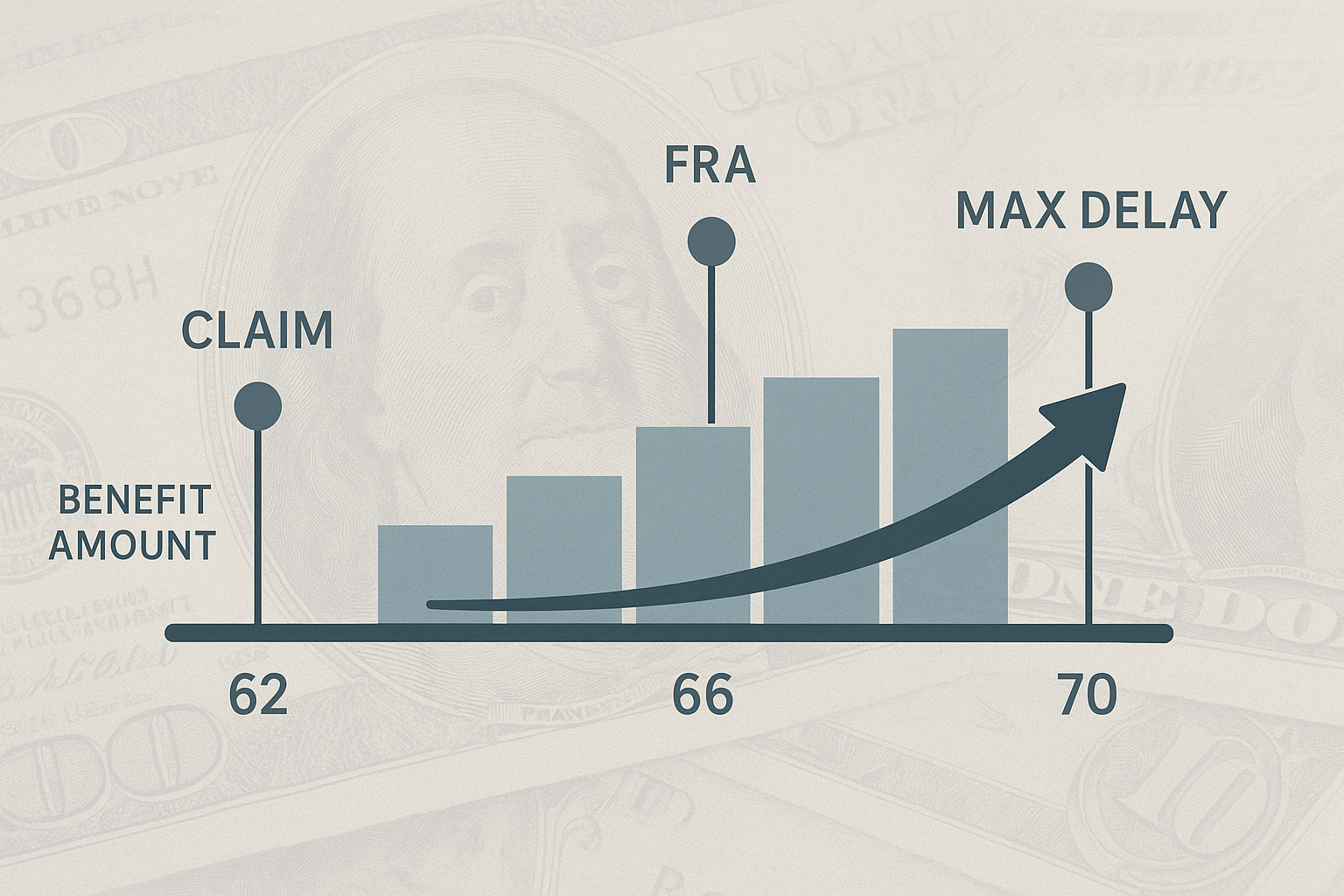

Understanding the Tradeoffs: Early Claiming vs. Delaying

This section lays out the simple math behind early vs. delayed claiming: starting benefits at 62 reduces the monthly amount, while delaying up to 70 increases monthly payments through delayed credits. We introduce break‑even analysis and present sample charts that compare cumulative received benefits across claiming ages. Readers are guided to use the included calculators and the downloadable Social Security timing worksheet to run their own scenarios, factoring in health, expected longevity, and other income sources.

Spouse and Survivor Strategies: Protecting Two Lives

A practical walkthrough of spousal and survivor benefit mechanics, including when a lower‑earning spouse might claim and when it can make sense for the higher‑earner to delay. The section includes stepwise numerical examples for couples with different earning histories and shows how survivor benefits can be the deciding factor for claiming choices. It emphasizes running couple‑level projections rather than single‑person analyses.

Working, Pensions, and Withdrawal Coordination

Explore how ongoing work before full retirement age can temporarily reduce monthly checks via the earnings test and how those withheld benefits are recalculated at FRA. We also show practical coordination tactics for households with defined benefit pensions or substantial 401(k)/IRA balances—how to think about sequencing withdrawals, taking pensions as a lump sum vs. annuity, and tax timing. Internal links are suggested to withdrawal sequencing and tax articles for deeper technical guidance.

Tools, Checklists, and Common Mistakes

This section lists the calculators and charts included with the guide (timing worksheet, break‑even calculator) and provides a step‑by‑step checklist for making a claiming decision. We highlight frequent errors—failing to coordinate spousal/survivor impacts, ignoring COLA updates, and not accounting for state taxes or WEP/GPO if applicable. The article closes with recommended next steps: run several scenarios, share results with your spouse, and consider booking a consultation if your situation is complex.

Frequently Asked Questions

What is the single most important factor in deciding when to claim Social Security?

The most important factor varies by household, but commonly it’s the balance between current income needs and the value of larger monthly payments later. Health, life expectancy, spousal/survivor protection, and other income sources also play key roles. Use break‑even analysis and scenario modeling to compare options for your situation.

Will working after I claim always reduce my Social Security benefits?

If you claim before full retirement age and earn above the annual earnings limit, Social Security may withhold some benefits temporarily under the earnings test. Withheld amounts are generally recalculated into higher monthly benefits starting at full retirement age. After full retirement age, there is no earnings test reduction. Check current annual limits, as they change periodically.

How do spousal and survivor benefits affect a couple’s claiming decision?

Spousal and survivor benefits can change the optimal claiming strategy because the surviving spouse’s income may depend on the higher earner’s benefit. Couples should model combined lifetime income and survivor outcomes—sometimes it makes sense for one spouse to delay to increase survivor protection even if that delays one spouse’s higher lifetime payout.

What is a break‑even analysis and why should I run one?

A break‑even analysis compares cumulative benefits received under different claiming ages to identify the age at which delaying benefits becomes financially superior to claiming earlier. It helps clarify the tradeoff between taking money sooner versus larger payments later, but it depends on assumptions about lifespan and discounting.

How should I coordinate Social Security with my pension and retirement accounts?

Coordination depends on the type and rules of your pension, the size of retirement accounts, tax implications, and cash‑flow needs. Common approaches include delaying Social Security while drawing from savings, or claiming Social Security early and preserving taxable assets. Use withdrawal sequencing and tax‑aware models (see linked resources) and consider professional advice for complex situations.

Related Articles in This Series

Plan Your Retirement Income With Confidence

If this topic raised questions about retirement income, taxes, market risk, or long-term planning, the next step is to review a simple educational guide and prepare for a strategy conversation.

Download the free guide: How to Maximize Social Security: Timing, Spousal/Survivor Benefits, and Strategies