Angle: Focus on worked numerical examples that compare different claiming combinations for couples and illustrate survivor outcomes.

How Spousal Benefits Are Calculated: A Clear Example

Step through a numerical example where one spouse has a higher PIA. Show how a lower‑earning spouse’s spousal benefit can be up to 50% of the higher earner’s PIA (subject to their own benefit amount and claiming age), and illustrate how claiming ages change those amounts. Emphasize checking SSA statements for precise estimates.

Survivor Benefits: Protecting the Surviving Spouse

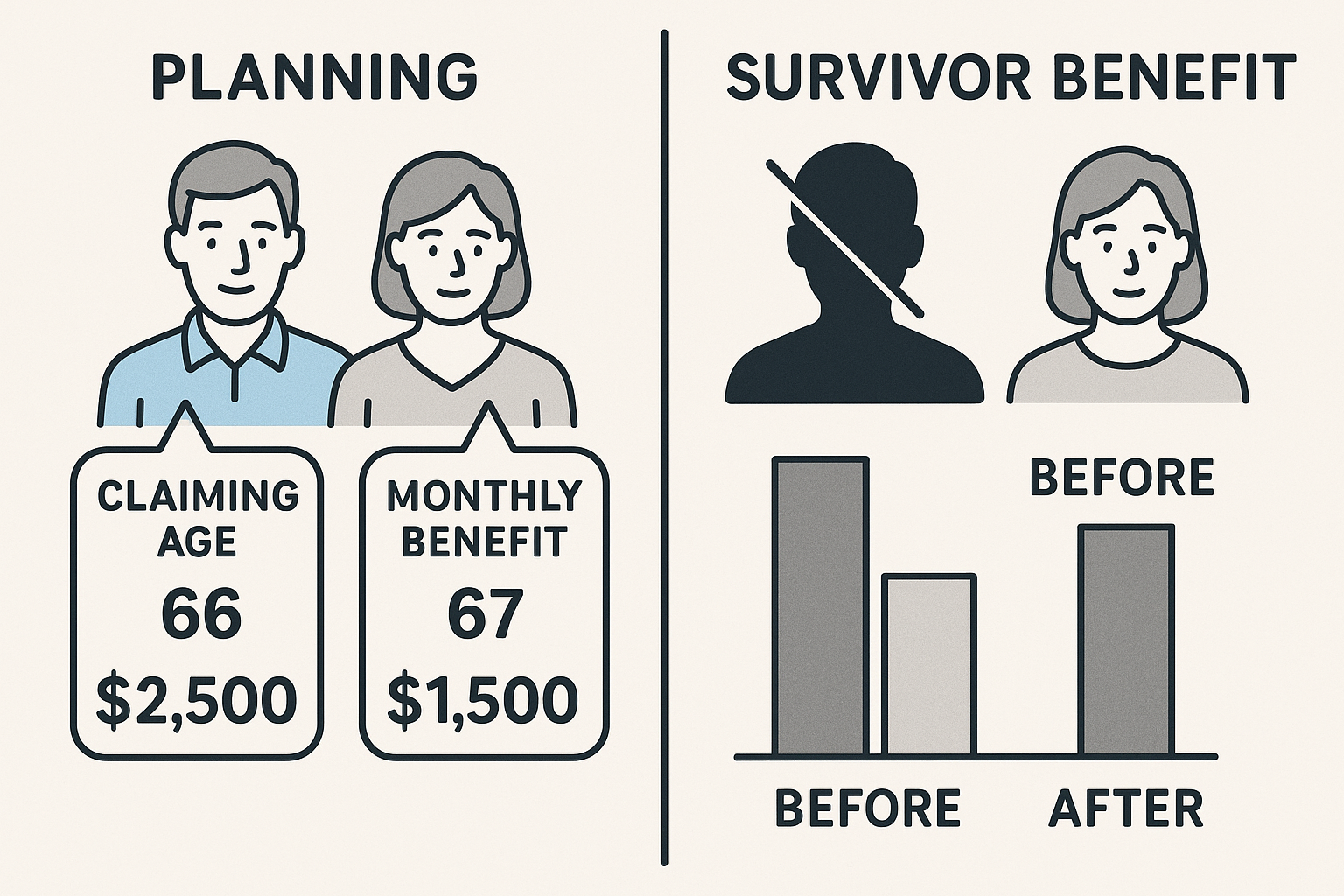

Provide a worked case showing a higher‑earner who delays and a lower‑earner who claims early. Show survivor benefit outcomes and how delaying the higher earner can increase the survivor’s future income. Explain the practical implications for couples with different health and longevity expectations.

Decision Framework for Couples: Comparing Lifetime and Survivor Income

Offer a framework to compare strategies: run couple‑level lifetime income projections, perform break‑even and sensitivity analyses for longevity and health changes, and consider insurance alternatives. Include a short checklist of items to gather (SSA statements, pension rules, current savings balances) before modeling.

Related Articles

Plan Your Retirement Income With Confidence

If this topic raised questions about retirement income, taxes, market risk, or long-term planning, the next step is to review a simple educational guide and prepare for a strategy conversation.

Download the free guide: How to Maximize Social Security: Timing, Spousal/Survivor Benefits, and Strategies