In This Series

In This Guide

Key Takeaways

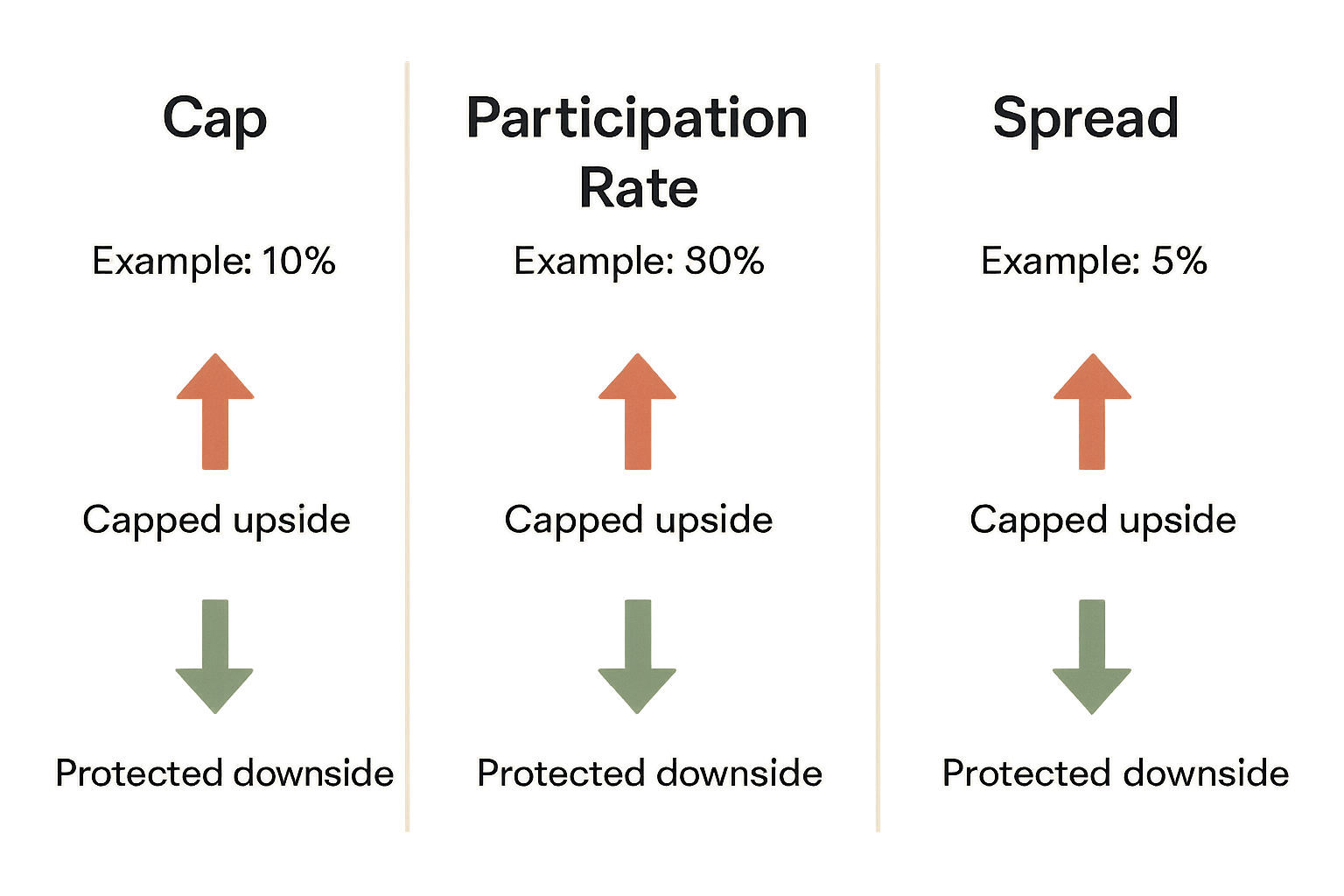

- Caps limit the maximum credited interest and can cap upside during strong markets

- Participation rates pass only a percentage of index gains to the contract, reducing potential credited interest

- Spreads subtract a fixed amount from index gains; all three methods reduce volatility while protecting against negative returns

Angle: Provide clear definitions and practical examples that show how each crediting method affects accumulation and income scenarios over time.

What caps mean for long-term growth

A cap sets a ceiling on the amount of index gain that will be credited in a given period. For example, if an index gains 15% and the contract has a cap of 8%, the credited interest for that period is limited to 8%. Caps produce predictable maximum credited gains but can materially reduce accumulation during prolonged bull markets. Over decades, higher caps generally translate into higher accumulated value if fees and other terms are comparable. When comparing IULs and FIAs, look at how insurers set caps across different crediting strategies and how often caps are reset, since these behaviors affect realistic growth expectations for retirement income planning.

How participation rates and spreads work

A participation rate credits a percentage of index performance to the contract. If the index gains 10% and the participation rate is 70%, the credited gain is 7%. Participation rates effectively share upside between the policyholder and the insurer. A spread subtracts a fixed percentage from index gains; for instance, a 2% spread on a 10% gain credits 8%. Both participation rates and spreads have the effect of reducing gross index upside and thus the long-term accumulation that will be available to generate retirement income. Products from different insurers can vary widely in how attractive these terms are, so reviewing historical scenario illustrations that include these mechanics helps set expectations.

Why these crediting mechanics matter for retirement income

Crediting mechanics directly affect how much value is available to support income later in life. A product with low caps or participation rates will likely produce less accumulated value than one with more generous crediting when index markets trend upward. However, similar crediting mechanisms across products also mean similar downside protection, since neither allows negative credited interest during most credited periods. For retirement income planning, match crediting features to time horizon and risk tolerance: longer time horizons may benefit from more generous upside credits, while shorter horizons often prioritize stronger downside guarantees. Readers who want to dig into how these mechanics interact with fees and liquidity can read the companion piece on fees, surrender charges, and liquidity considerations.

Related Articles

- IULs vs Fixed Indexed Annuities for retirement income: How to Compare the Two

- Liquidity, fees, and surrender charges: what retirees need to know

- Designing predictable retirement income: income riders, annuitization, and policy loans

- 7 Retirement Risks That Could Derail Your Retirement Plan

- Implementing IUL Strategies for Retirement Income: Design, Risks, and Steps

- 401k Retirement Income Strategy: How to Turn Savings Into a Reliable Paycheck

About the Author

John P. Sansaricq is a licensed insurance professional focused on retirement income planning, life insurance strategies, and educational resources for pre-retirees and retirees.

He helps individuals and families explore ways to protect savings, manage risk, and prepare for more informed retirement planning conversations.

Plan Your Retirement Income With Confidence

If this topic raised questions about retirement income, taxes, market risk, or long-term planning, the next step is to review a simple educational guide and prepare for a strategy conversation.

Download the free guide: IULs vs Fixed Indexed Annuities for Retirement Income: A Practical Guide for U.S. Families and Retirees