In This Series

In This Guide

Key Takeaways

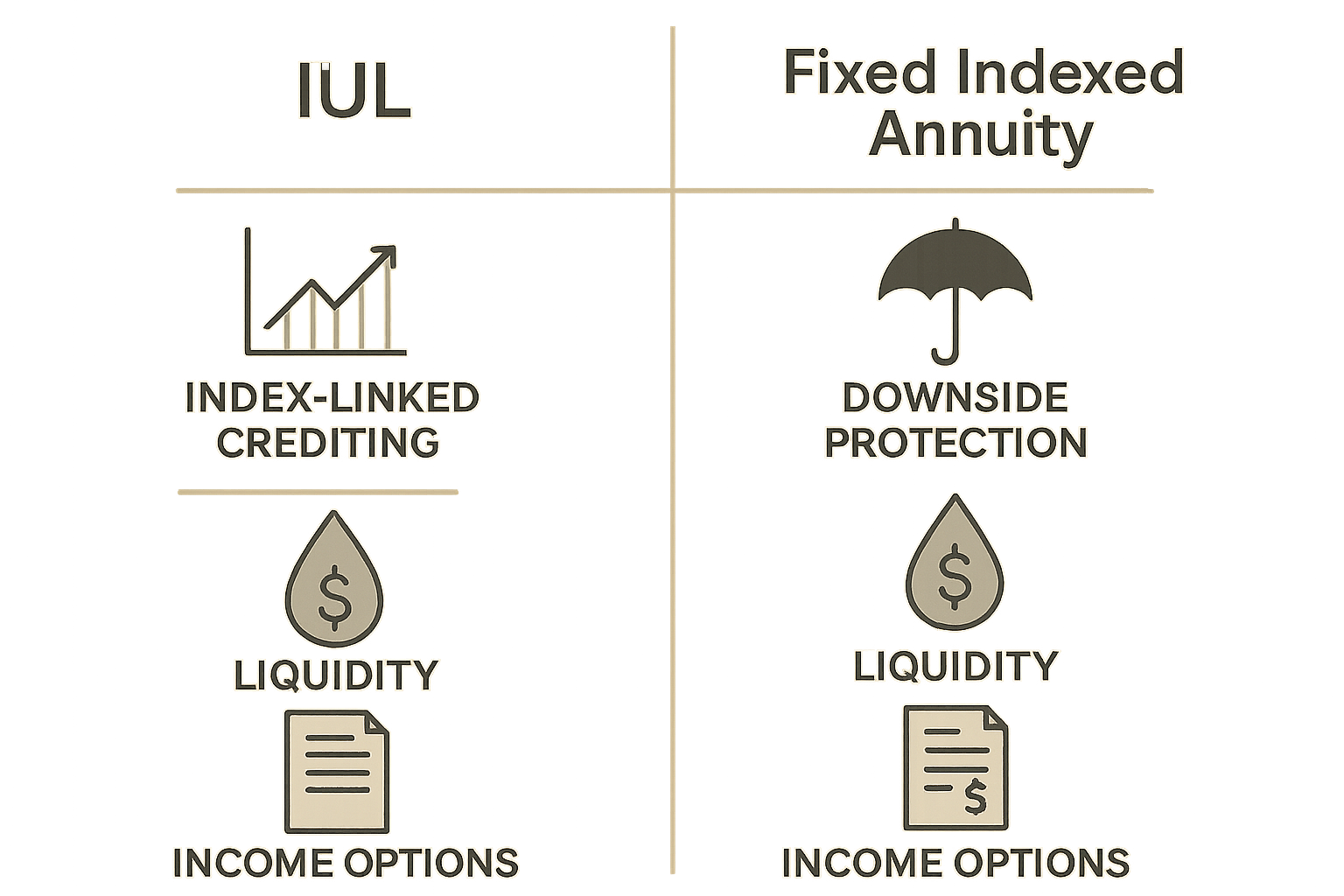

- Both IULs and FIAs link credited interest to index performance but limit downside in different ways

- IULs combine life insurance and cash value with loan/withdrawal access while FIAs focus on accumulation and conversion to income

- Fees, surrender charges, and crediting mechanisms significantly affect long-term income potential

How both products credit index-linked interest

Indexed Universal Life policies and Fixed Indexed Annuities typically credit interest based on an external market index without directly investing in the index. Insurers use crediting methods such as caps, participation rates, and spreads to determine the amount of the market gain passed through to the contract. A cap limits the maximum credited interest, a participation rate applies a percentage of the index gain, and a spread subtracts a fixed percentage from gains. Both product types may offer guaranteed minimums that prevent negative credited interest during down periods, but those guarantees vary by contract and are tied to the insurer's claims-paying ability. Understanding these mechanics is essential because they determine realistic upside and how income potential accumulates over time.

Access, liquidity, and policy mechanics that affect income

Accessing value differs between IULs and FIAs. IULs typically permit policy loans and partial withdrawals from the cash value. Loans are often income-tax-free if managed according to current tax rules and if the policy remains in force, but loan interest and loan balances reduce cash value and death benefits. FIAs generally offer penalty-free withdrawals up to a modest annual percentage and have surrender charges if funds are taken out during early contract years. Both IULs and FIAs can include features that convert accumulated value into lifetime income: IULs do this indirectly through loans or structured withdrawals while maintaining a death benefit, and FIAs commonly offer annuitization or income riders designed to produce predictable lifetime payments. The relative importance of liquidity versus guaranteed income should guide how each product might fit into a retirement strategy.

Costs, fees, and transparency to consider

Costs show up differently. IULs disclose insurance-related charges such as the cost of insurance (COI), administrative fees, and loan interest. Those costs can increase with age or changes in the underlying mortality assumptions. FIAs present surrender schedules, market value adjustment features in some contracts, and rider costs when income guarantees are added. Rider fees for income guarantees reduce credited interest or accumulate as explicit charges. Comparing apples to apples requires reviewing illustrations that show net accumulation after assumed crediting and fees, and understanding the assumptions behind those illustrations. Because products vary widely, transparency in how features affect long-term income is a key comparison point.

Putting it together for retirement income planning

Deciding between IULs vs Fixed Indexed Annuities for retirement income depends on priorities. If maintaining a death benefit for beneficiaries alongside flexible access to cash value is important, IULs can be relevant; if converting accumulated value into predictable lifetime income is the priority, FIAs with income riders or annuitization paths might better match that singular objective. Many households find that a mix of instruments—tax-advantaged accounts, safe-bucket investments, FIAs for guaranteed income, and, where appropriate, IULs for legacy purposes—creates balance. Use realistic scenario illustrations to see how crediting mechanics, fees, and withdrawals interact over decades. This article complements deeper dives on topics like caps and participation rates, liquidity and surrender charges, and income rider mechanics that appear in the companion articles within this series.

Frequently Asked Questions

Are Indexed Universal Life policies and Fixed Indexed Annuities insured by the same protections?

Both products are insurance contracts backed by the financial strength of the issuing insurer. State guaranty associations provide limited protection for policyholders in the event of insurer insolvency, but coverage limits vary by state and by product type. Check your state’s guaranty association rules and review an insurer’s financial ratings for an assessment of claims-paying ability.

Can I use an IUL or FIA for guaranteed lifetime income?

FIAs are commonly structured to create guaranteed lifetime income through annuitization or income riders. IULs can support lifetime income via policy loans or structured withdrawals, and some may offer riders that affect income or death benefits, but the mechanics and guarantees differ. Understanding the contract specifics, fees, and long-term effects on cash value and death benefit is essential when considering either product for income.

How do surrender charges and loan interest affect retirement income planning?

Surrender charges reduce the amount available if funds are withdrawn from an annuity during the surrender period, potentially lowering short-term liquidity. Loan interest on IULs accrues and can reduce cash value and death benefit if not repaid. Both elements can materially change the amount of income available and should be included in scenario illustrations used for retirement planning. This content is educational and not tax, legal, or investment advice.

Related Articles in This Series

- How caps, participation rates, and spreads shape IUL and FIA returns

- Liquidity, fees, and surrender charges: what retirees need to know

- Designing predictable retirement income: income riders, annuitization, and policy loans

- 401k Retirement Income Strategy: How to Turn Savings Into a Reliable Paycheck

- Implementing IUL Strategies for Retirement Income: Design, Risks, and Steps

- 7 Retirement Risks That Could Derail Your Retirement Plan

About the Author

John P. Sansaricq is a licensed insurance professional focused on retirement income planning, life insurance strategies, and educational resources for pre-retirees and retirees.

He helps individuals and families explore ways to protect savings, manage risk, and prepare for more informed retirement planning conversations.

Plan Your Retirement Income With Confidence

If this topic raised questions about retirement income, taxes, market risk, or long-term planning, the next step is to review a simple educational guide and prepare for a strategy conversation.

Download the free guide: IULs vs Fixed Indexed Annuities for Retirement Income: A Practical Guide for U.S. Families and Retirees