In This Series

In This Guide

Key Takeaways

- IUL loans and withdrawals affect cash value and death benefit and carry loan interest

- FIAs often impose surrender charges during early contract years and limit penalty-free withdrawals annually

- Comparing net illustrated accumulation after fees and potential charges provides a clearer view of available retirement income

Angle: Focus on real-life examples of withdrawals, loans, and surrender periods to illustrate the impact of fees and penalties on retirement income planning.

IUL liquidity: loans, withdrawals, and their effects

Indexed Universal Life policies typically allow policy loans and partial withdrawals from cash value. Policy loans can be attractive because they are commonly treated as income tax-free when the policy remains in force and is structured correctly, but loan interest accrues and unpaid loans reduce cash value and death benefit. Withdrawals may reduce the cost basis and could create taxable events in some situations. Behavior matters: using loans to fund retirement income can work, but the interaction of loan interest, credited interest, and insurance costs must be monitored to avoid policy lapse, which can create taxable consequences. Illustrations that model loan scenarios across market cycles help households see potential outcomes.

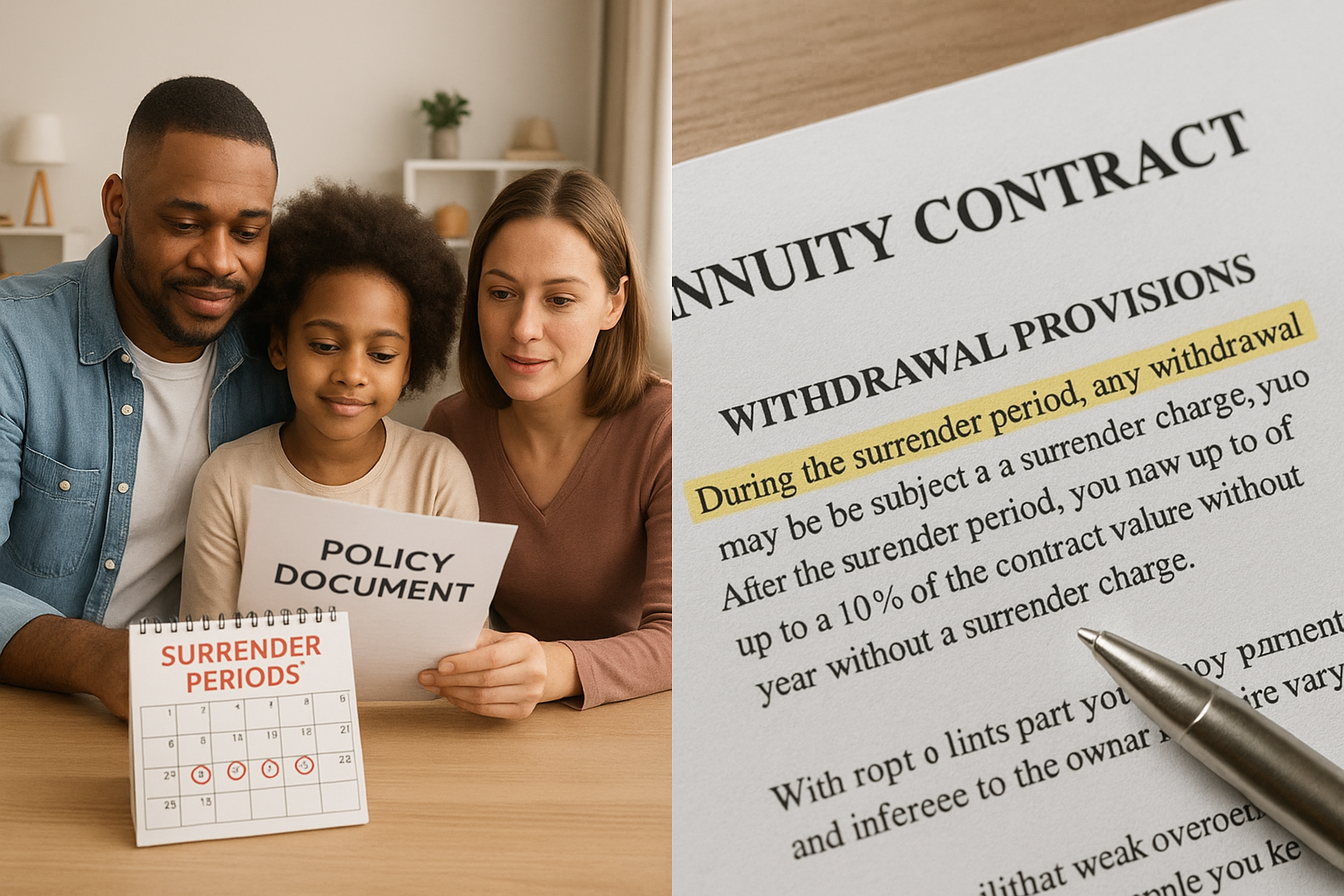

Fixed Indexed Annuity liquidity and surrender charges

Fixed Indexed Annuities often include surrender schedules that impose charges for early withdrawals during the initial contract years. Many FIAs permit penalty-free withdrawals up to a stated percentage—commonly 5% to 10% annually—while larger distributions may incur surrender penalties or market value adjustments. Some FIAs offer liquidity riders or features for long-term care or other needs but these can add cost. For retirement income planning, it is important to know the surrender period length, the penalty structure, and any contract restrictions on frequency and timing of withdrawals because surrender charges can materially reduce the funds available during the critical early withdrawal years.

Fees, transparency, and comparing net outcomes

Both product families have fees, but they appear differently on statements and illustrations. IULs present COI charges, administrative fees, and loan interest, while FIAs disclose rider fees, surrender schedules, and any market value adjustments. Comparing gross credited rates without subtracting fees can be misleading; instead, review net-projected outcomes under reasonable scenario assumptions, including prolonged market downturns and regular withdrawals. Work with a licensed professional to obtain conservative illustrations and sensitivity examples. Remember that this article is educational and not tax, legal, or investment advice.

Related Articles

- IULs vs Fixed Indexed Annuities for retirement income: How to Compare the Two

- How caps, participation rates, and spreads shape IUL and FIA returns

- Designing predictable retirement income: income riders, annuitization, and policy loans

- Implementing IUL Strategies for Retirement Income: Design, Risks, and Steps

- 401k Retirement Income Strategy: How to Turn Savings Into a Reliable Paycheck

- 7 Retirement Risks That Could Derail Your Retirement Plan

About the Author

John P. Sansaricq is a licensed insurance professional focused on retirement income planning, life insurance strategies, and educational resources for pre-retirees and retirees.

He helps individuals and families explore ways to protect savings, manage risk, and prepare for more informed retirement planning conversations.

Plan Your Retirement Income With Confidence

If this topic raised questions about retirement income, taxes, market risk, or long-term planning, the next step is to review a simple educational guide and prepare for a strategy conversation.

Download the free guide: IULs vs Fixed Indexed Annuities for Retirement Income: A Practical Guide for U.S. Families and Retirees