In This Series

In This Guide

Key Takeaways

- Indexing strategies determine how the interest credited to an FIA is calculated based on a market index's performance.

- Common strategies include point-to-point, annual reset, and monthly averaging, each with distinct advantages and calculations.

- Caps, participation rates, and spreads are key mechanisms that limit the amount of market-linked gain an FIA can capture.

- Understanding these indexing mechanics is crucial for evaluating and comparing different Fixed Indexed Annuity products.

Angle: This article focuses on the technical aspects of how interest is credited in FIAs, breaking down different indexing strategies and their associated mechanics.

The Basics of FIA Indexing

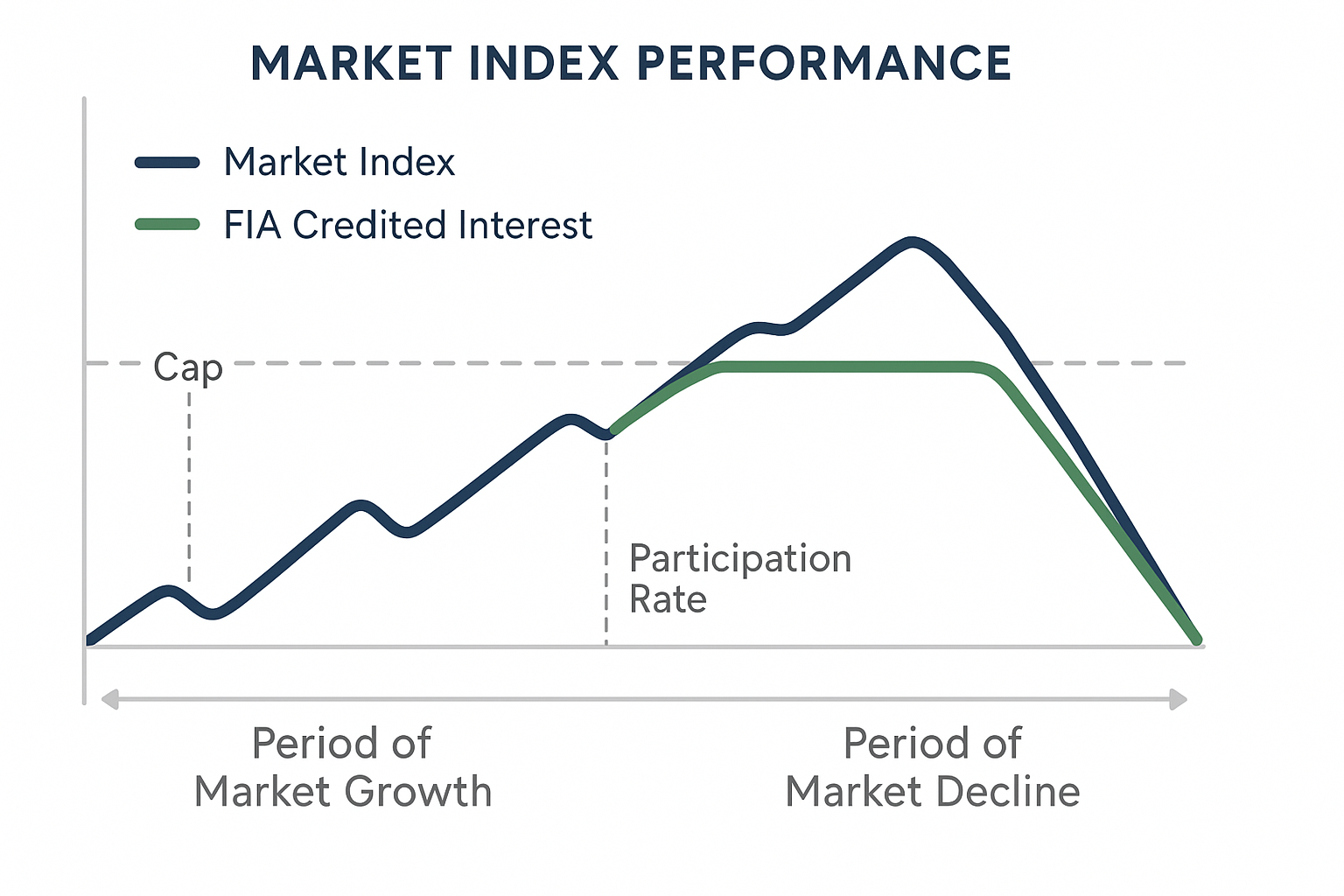

At its core, an FIA's growth is tied to the performance of an external market index, such as the S&P 500 or NASDAQ 100, without directly investing in the securities of that index. Instead of receiving dividends or direct stock returns, the annuity credits interest based on a portion of the index's positive movement. This design provides principal protection, meaning your initial premium is not at risk of market downturns. However, to offer this protection and ensure profitability for the insurance company, the growth potential is typically limited by specific mechanisms. These limitations are integral to the indexing strategy and include caps, participation rates, and spreads, which we will explore in detail.

Common Indexing Strategies Explained

Different FIAs utilize various indexing strategies, each with its own method for calculating interest. The 'point-to-point' strategy compares the index value at the beginning of a contract period to its value at the end. If there's a gain, interest is credited based on that gain, subject to caps or participation rates. The 'annual reset' (or 'ratchet') strategy measures the index's performance annually, locking in any gains each year and preventing previous gains from being lost in subsequent downturns. The 'monthly averaging' strategy calculates interest based on the average of the index's values over a specified period, often monthly, which can smooth out market volatility. Each strategy has implications for how much growth you might capture, and understanding these differences is vital when considering using Fixed Indexed Annuities for guaranteed income.

Understanding Caps, Participation Rates, and Spreads

To manage risk and provide principal protection, Fixed Indexed Annuities employ limiting factors. A 'cap rate' is the maximum percentage of interest that can be credited to your annuity in a given period, regardless of how high the index performs. For example, if the index gains 15% but your cap is 8%, you'll receive 8% interest. A 'participation rate' is the percentage of the index's gain that is applied to your annuity. If the index gains 10% and your participation rate is 70%, you'll receive 7% interest. A 'spread' or 'administrative fee' is a percentage deducted from the index's gain before interest is credited. For instance, if the index gains 10% and there's a 2% spread, you'd be credited interest on an 8% gain (subject to any caps). These mechanisms are fundamental to how FIAs work and directly impact your potential returns, making a clear understanding of them essential for prospective annuitants.

Related Articles

- Using Fixed Indexed Annuities for Guaranteed Income - A Comprehensive Guide

- Fixed Indexed Annuities vs. Other Retirement Income Options

- When Should You Take Social Security? (62 vs 67 vs 70) — How to Compare Your Options

- Tired Landlord Retirement Income Alternatives: How to Turn Rentals Into Predictable Retirement Cash Flow

- How Inflation Quietly Destroys Retirement Income: What Retirees Need to Know

- 401k Retirement Income Strategy: How to Turn Savings Into a Reliable Paycheck

About the Author

John P. Sansaricq is a licensed insurance professional focused on retirement income planning, life insurance strategies, and educational resources for pre-retirees and retirees.

He helps individuals and families explore ways to protect savings, manage risk, and prepare for more informed retirement planning conversations.

Plan Your Retirement Income With Confidence

If this topic raised questions about retirement income, taxes, market risk, or long-term planning, the next step is to review a simple educational guide and prepare for a strategy conversation.

Download the free guide: Your Guide to Fixed Indexed Annuities for Retirement Income