In This Series

In This Guide

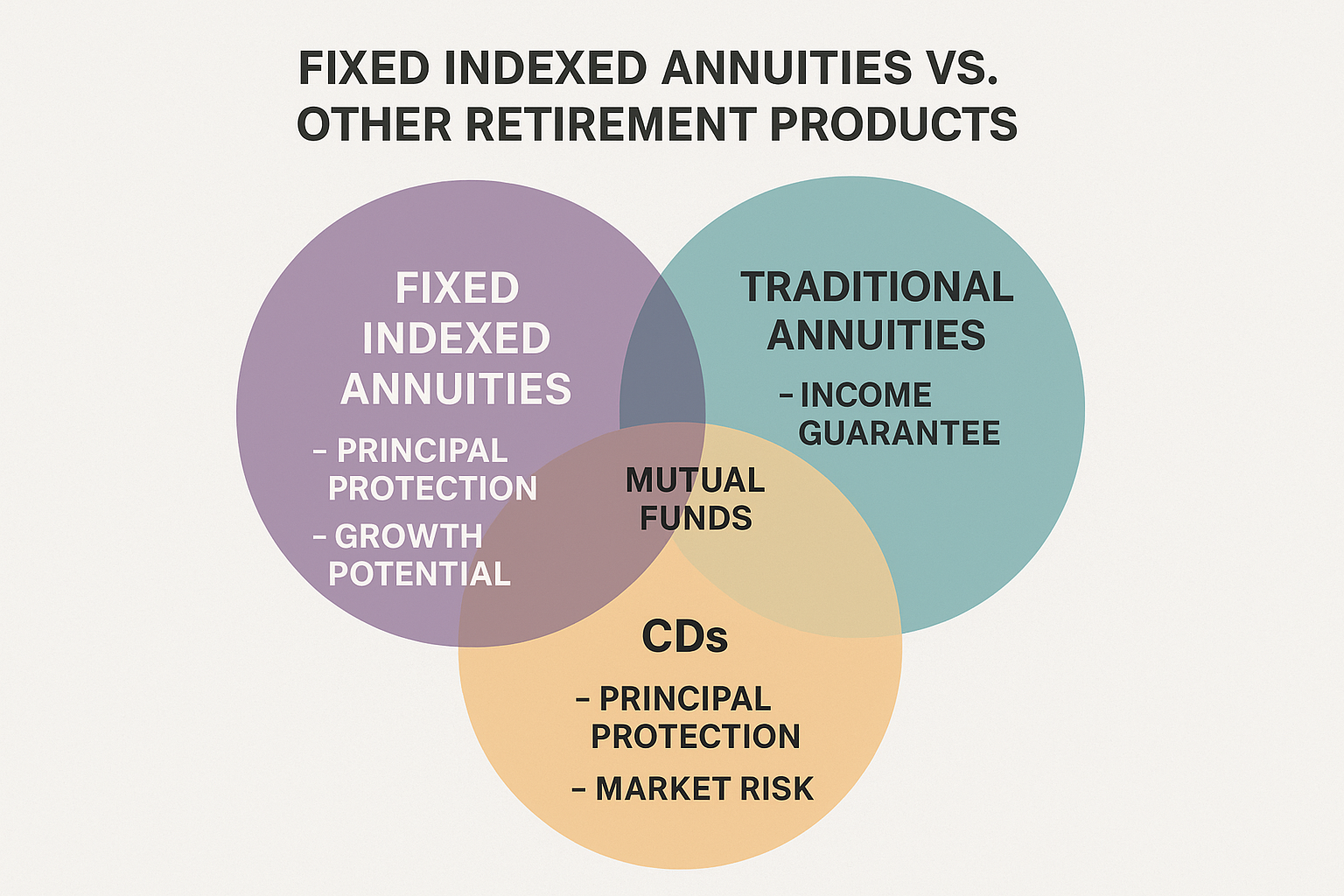

Key Takeaways

- Fixed Indexed Annuities offer a unique blend of principal protection and market-linked growth potential, setting them apart from many other options.

- Unlike traditional fixed annuities, FIAs can provide higher growth potential, while differing from variable annuities by protecting principal from market downturns.

- FIAs provide principal protection not found in direct market investments like mutual funds, though with capped growth potential.

- Compared to low-risk options like CDs, FIAs generally offer greater growth potential over the long term, albeit with less liquidity.

Angle: This article provides a comparative analysis of FIAs against other common retirement income tools, highlighting their unique position.

FIAs Compared to Traditional Fixed and Variable Annuities

When considering annuities, it's helpful to differentiate Fixed Indexed Annuities from their traditional counterparts. A 'traditional fixed annuity' offers a guaranteed interest rate for a set period, providing predictable but often conservative growth. FIAs, by contrast, offer growth potential tied to a market index, which can lead to higher returns than fixed annuities during periods of market growth, while still protecting principal. 'Variable annuities' offer direct investment in sub-accounts similar to mutual funds, providing potentially higher returns but also exposing the principal to market risk. The key distinction is that FIAs aim for a middle ground: market-linked growth potential without the direct market risk to principal that variable annuities carry, making them a distinct choice for those using Fixed Indexed Annuities for guaranteed income.

How FIAs Differ from Market Investments (Stocks, Mutual Funds)

Direct market investments like stocks and mutual funds offer the potential for significant growth, as you fully participate in market upside. However, they also come with inherent market risk, meaning your principal can decrease in value during market downturns. Fixed Indexed Annuities, on the other hand, prioritize principal protection. While they offer market-linked growth potential, this growth is typically capped or subject to participation rates, meaning you won't capture 100% of the index's gains. This trade-off between unlimited upside potential (with risk) and limited upside potential (with principal protection) is a crucial differentiator. For individuals who are nearing retirement or are risk-averse, the security offered by an FIA can be more appealing than the volatility of direct market investments, especially when seeking a reliable income source.

FIAs Alongside Other Low-Risk Options (CDs, Money Market)

For those seeking low-risk options, Certificates of Deposit (CDs) and money market accounts are common choices. CDs offer a fixed interest rate for a specific term, and money market accounts provide liquidity with modest interest earnings. Both are generally very low-risk, with FDIC insurance protecting deposits up to certain limits. Fixed Indexed Annuities share the low-risk characteristic of principal protection, but they aim to provide greater growth potential than typical CDs or money market accounts by linking interest to a market index. While FIAs are not FDIC-insured, they are backed by the financial strength of the issuing insurance company. The trade-off is often liquidity; FIAs are designed for long-term savings and typically have surrender charges, whereas CDs and money market accounts generally offer more accessible funds. This makes FIAs a consideration for a portion of your retirement savings where you prioritize long-term growth with principal protection over immediate access to funds, complementing other low-risk vehicles in a diversified portfolio.

Related Articles

- Using Fixed Indexed Annuities for Guaranteed Income - A Comprehensive Guide

- Understanding Fixed Indexed Annuity Indexing Strategies

- The 401(k) Tax Trap Most Retirees Don’t See Coming — What It Is and How to Respond

- 7 Retirement Risks That Could Derail Your Retirement Plan

- When Should You Take Social Security? (62 vs 67 vs 70) — How to Compare Your Options

- IULs vs Fixed Indexed Annuities for retirement income: How to Compare the Two

About the Author

John P. Sansaricq is a licensed insurance professional focused on retirement income planning, life insurance strategies, and educational resources for pre-retirees and retirees.

He helps individuals and families explore ways to protect savings, manage risk, and prepare for more informed retirement planning conversations.

Plan Your Retirement Income With Confidence

If this topic raised questions about retirement income, taxes, market risk, or long-term planning, the next step is to review a simple educational guide and prepare for a strategy conversation.

Download the free guide: Your Guide to Fixed Indexed Annuities for Retirement Income