In This Series

In This Guide

Key Takeaways

- Sequencing withdrawals can prevent unnecessary spikes in taxable income and avoid IRMAA-related premium increases.

- A flexible plan uses taxable accounts first, converts modest 401(k) amounts to Roth in low years, and preserves Roth for later tax-free access.

- Regularly revisiting the sequence as income and tax rules change keeps the plan aligned with retirement goals.

Angle: Provide a step-by-step, adaptable method for sequencing withdrawals that considers tax brackets, Medicare IRMAA thresholds, and the timing of Social Security benefits.

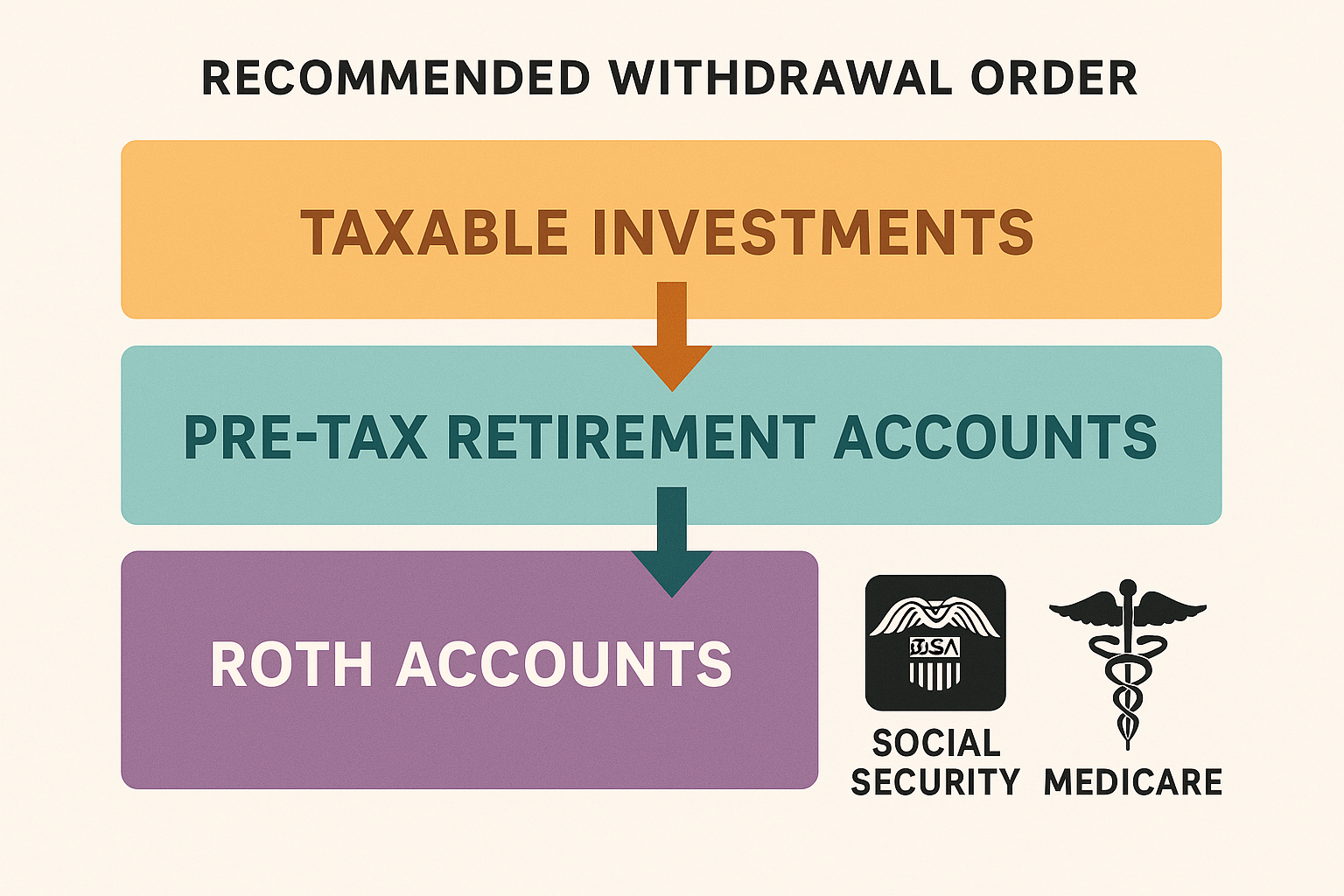

Principles of Tax-Aware Withdrawal Sequencing

Tax-aware sequencing relies on the relative tax treatment of account types. Taxable accounts provide capital gains and basis management options, pre-tax accounts create ordinary income at distribution, and Roth accounts offer tax-free withdrawals. Using taxable resources early allows a retiree to avoid realizing large ordinary income amounts in years when Social Security or other income begins, while selective Roth conversions in low-income years can create future tax-free flexibility.

A Practical Sequencing Framework

A common framework begins with taxable account withdrawals to preserve low taxable income years for Roth conversions, followed by a mix of partial Roth conversions and controlled 401(k) distributions. Roth funds are generally reserved for later-stage withdrawals or years with high medical or long-term care expenses. This framework aims to smooth taxable income, protect means-tested benefits, and adapt to changing tax brackets and market returns.

Monitoring, Adjusting, and Integrating with Broader Planning

Sequencing is not a one-time decision. Annual reviews of income projections, market performance, and any changes to Social Security or Medicare status are essential. Integrating sequencing decisions with estate planning, beneficiary designations, and charitable goals supports a coherent retirement plan and helps avoid the worst of the 401(k) tax trap illustrated in 'The 401(k) Tax Trap Most Retirees Don’t See Coming.'

Related Articles

- The 401(k) Tax Trap Most Retirees Don’t See Coming — What It Is and How to Respond

- Roth Conversions Without the Sticker Shock

- RMDs and Your 401(k): Avoiding Last-Minute Tax Surprises

- Implementing IUL Strategies for Retirement Income: Design, Risks, and Steps

- 7 Retirement Risks That Could Derail Your Retirement Plan

- 401k Retirement Income Strategy: How to Turn Savings Into a Reliable Paycheck

About the Author

John P. Sansaricq is a licensed insurance professional focused on retirement income planning, life insurance strategies, and educational resources for pre-retirees and retirees.

He helps individuals and families explore ways to protect savings, manage risk, and prepare for more informed retirement planning conversations.

Plan Your Retirement Income With Confidence

If this topic raised questions about retirement income, taxes, market risk, or long-term planning, the next step is to review a simple educational guide and prepare for a strategy conversation.

Download the free guide: The 401(k) Tax Trap Most Retirees Don’t See Coming: A Practical Guide