In This Series

In This Guide

Key Takeaways

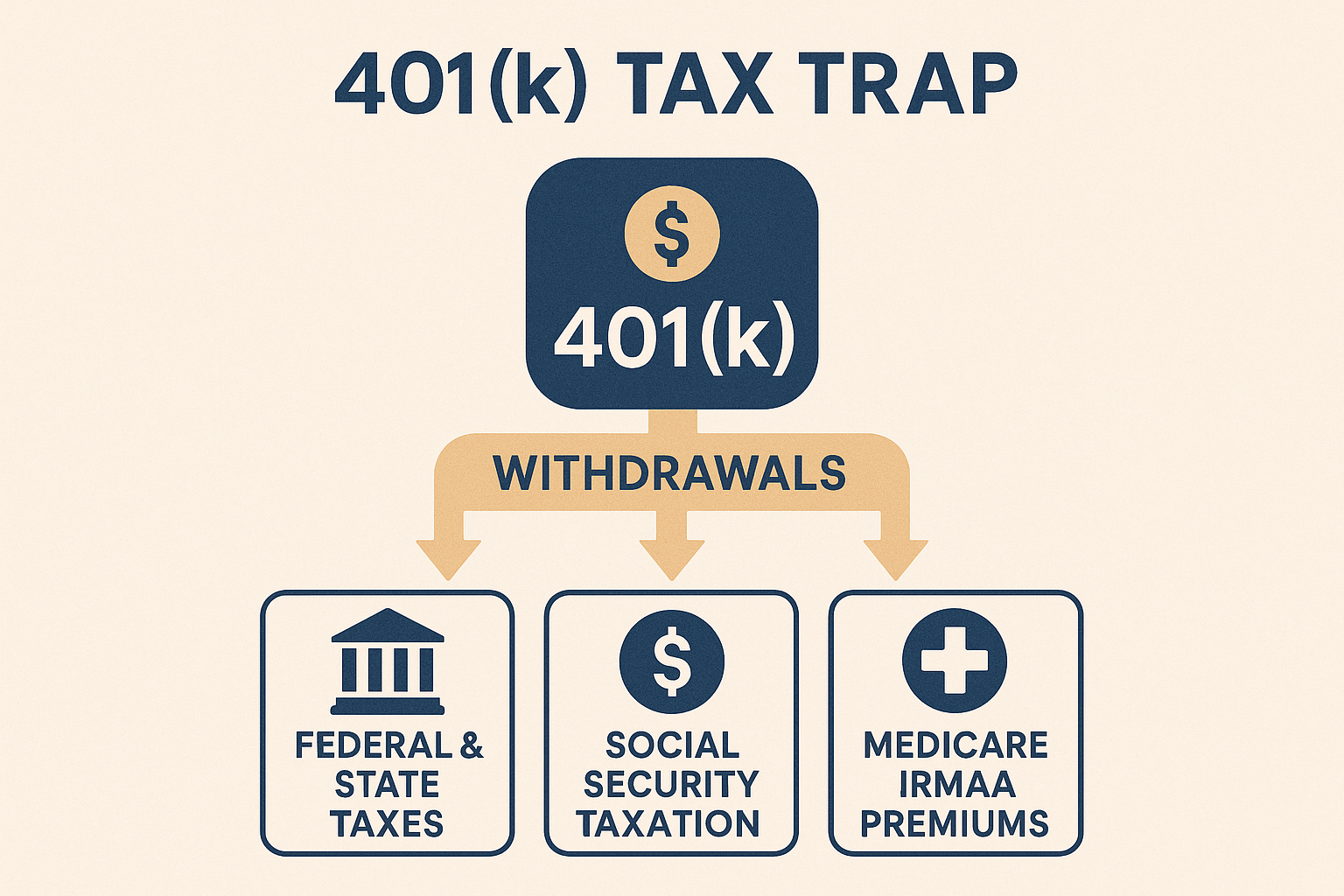

- Pre-tax 401(k) withdrawals count as ordinary income and can trigger higher federal and state taxes as well as Medicare surcharges.

- Tax diversification — holding taxable, tax-deferred, and tax-free accounts — reduces the chance of large tax-driven income spikes.

- Partial Roth conversions and careful withdrawal sequencing can spread tax obligations and protect benefits like Medicare and Social Security.

How the Tax Trap Develops

A tax trap often starts with an accumulation decision made years earlier: contributions to a traditional 401(k) delivered tax deferral and lower taxable income while working. In retirement, withdrawals from that account are taxed as ordinary income, which means a single large withdrawal or a stream of required minimum distributions can materially change a retiree’s tax picture. When taxable income rises, the ripple effects include higher marginal tax rates, increased taxation of Social Security benefits, and potential IRMAA surcharges that raise Medicare Part B and Part D premiums. The cumulative impact can reduce net household income in a way that was not fully anticipated when planning for retirement.

Why Many Retirees Miss the Warning Signs

Statements from 401(k) plans rarely show how future distributions will interact with Social Security and Medicare. Many retirees focus on account balances and withdrawal rates without connecting those withdrawals to the tax forms filed each year. Events such as rolling multiple employer plans into a single pre-tax account, taking a large one-time withdrawal, or beginning required minimum distributions can create sudden jumps in taxable income. Recognizing these warning signs early—by modeling expected taxable income under multiple scenarios—reduces the chance that taxes or benefit cliffs will arrive as a surprise.

Practical Strategies to Reduce Tax Shock

A range of practical strategies helps manage the 401(k) tax trap. Tax diversification spreads retirement savings across taxable, tax-deferred, and tax-free (Roth) buckets so future withdrawals can be sequenced to limit taxable income. Partial Roth conversions convert manageable portions of a 401(k) into Roth accounts during years with lower taxable income, allowing tax-free growth and tax-free withdrawals later. Charitable approaches, such as qualified charitable distributions for those over the eligible age, can reduce taxable income while supporting philanthropic goals. These strategies should be integrated into a full-year income projection and adjusted as life events, market returns, and tax rules change.

Coordinating Withdrawals with Benefits and Life Events

Withdrawal sequencing coordinates the timing and source of distributions with Social Security claiming, Medicare enrollment, and other benefit-sensitive dates. For example, delaying Social Security while using taxable accounts first could keep taxable income lower in early retirement and create an opportunity for Roth conversions at favorable tax rates. Conversely, taking large pre-tax 401(k) distributions in the same years that Social Security begins or that required minimum distributions start can create compounded costs. Regularly reviewing cash flow projections and consulting companion resources such as 'Roth Conversions Without the Sticker Shock' and 'RMDs and Your 401(k): Avoiding Last-Minute Tax Surprises' helps build a cohesive plan.

Frequently Asked Questions

What exactly is the 401(k) tax trap many retirees face?

The tax trap occurs when large pre-tax 401(k) withdrawals or required minimum distributions create spikes in taxable income. Those spikes can push retirees into higher tax brackets, increase taxation of Social Security benefits, and trigger higher Medicare Part B and D premiums through IRMAA adjustments, all of which reduce after-tax retirement income.

Will converting my 401(k) to a Roth eliminate future taxes?

Converting to a Roth means taxes are paid on the converted amount in the year of conversion, while qualified Roth withdrawals are generally tax-free later. Conversions can reduce future taxable required distributions, but they create current tax liability and should be spread across years to avoid pushing a single year’s income too high. This content is educational and not a substitute for personalized tax advice.

How does withdrawal sequencing help reduce Medicare premium increases?

Sequencing withdrawals to keep reported taxable income lower in years when Medicare premiums are calculated can reduce the chance of triggering IRMAA surcharges. Using taxable accounts earlier, timing Roth conversions in years with low income, and managing Social Security claiming age are common sequencing tactics that can affect Medicare premiums and overall tax exposure.

Are qualified charitable distributions (QCDs) a useful tool to avoid the tax trap?

Qualified charitable distributions allow eligible retirees to transfer IRA funds directly to qualified charities without counting the amount as taxable income. QCDs can lower taxable income and help manage the size of required minimum distributions, which may reduce tax-related impacts. Eligibility, limits, and rules should be reviewed with a tax professional.

Related Articles in This Series

- Roth Conversions Without the Sticker Shock

- RMDs and Your 401(k): Avoiding Last-Minute Tax Surprises

- Withdrawal Sequencing to Minimize Taxes and Medicare Premium Hits

- Implementing IUL Strategies for Retirement Income: Design, Risks, and Steps

- 7 Retirement Risks That Could Derail Your Retirement Plan

- IULs vs Fixed Indexed Annuities for retirement income: How to Compare the Two

About the Author

John P. Sansaricq is a licensed insurance professional focused on retirement income planning, life insurance strategies, and educational resources for pre-retirees and retirees.

He helps individuals and families explore ways to protect savings, manage risk, and prepare for more informed retirement planning conversations.

Plan Your Retirement Income With Confidence

If this topic raised questions about retirement income, taxes, market risk, or long-term planning, the next step is to review a simple educational guide and prepare for a strategy conversation.

Download the free guide: The 401(k) Tax Trap Most Retirees Don’t See Coming: A Practical Guide