In This Series

In This Guide

Key Takeaways

- Dynamic withdrawal rules adapt spending to portfolio performance, improving sustainability compared with rigid inflation adjustments

- Spending bands and percentage-of-portfolio rules offer balanced trade-offs between stability and longevity

- Budgeting tools that separate essential and discretionary expenses make it easier to adjust spending when conditions change

Angle: An action-oriented look at withdrawal flexibility, including step-down and step-up rules, spending bands tied to portfolio thresholds, and budgeting practices that support long-term sustainability.

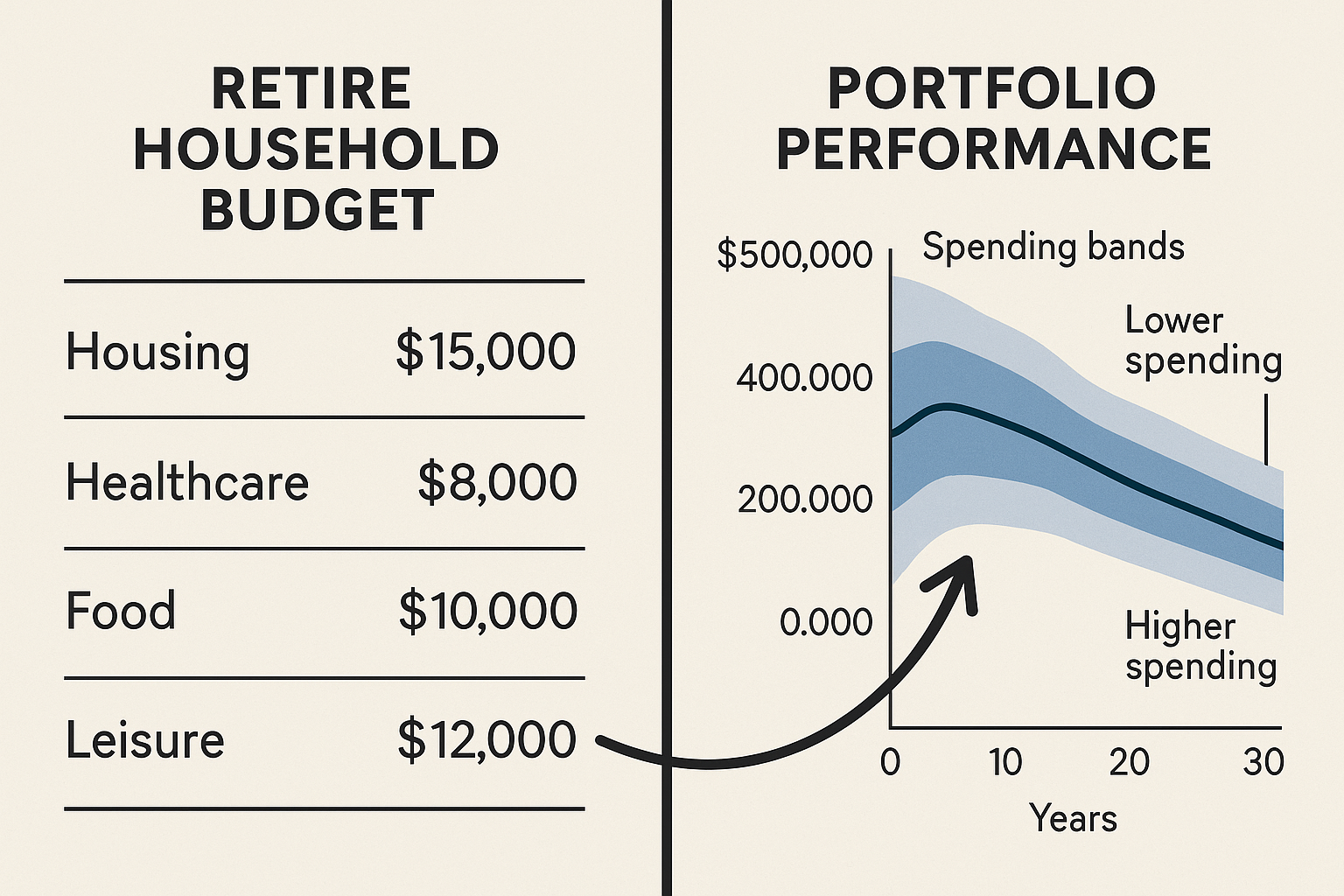

Types of Dynamic Withdrawal Rules

Dynamic withdrawal rules include percentage-of-portfolio methods, spending bands, and rules that adjust inflation-linked withdrawals based on market performance. Percentage-of-portfolio withdrawals pay a fixed share of portfolio value each year, so payments naturally fall in bear markets and rise in bull markets. Spending bands set a target payment with upper and lower thresholds that trigger modest changes only when the portfolio changes materially. Other rules delay adjustments for a set period after sharp market moves, giving time for recovery before cuts.

Linking Withdrawals to a Household Budget

Breaking spending into essential and discretionary categories clarifies where cuts can be made without undermining basic needs. Essentials should be covered by reliable income sources or conservative withdrawal plans, while discretionary spending can be adjusted more frequently. Monthly and annual budgeting tools that track spending versus withdrawals make it easier to enact temporary reductions or increases without emotional stress during volatile market periods.

Operational Steps to Implement Dynamic Strategies

Operationally, families can set an initial withdrawal rule, create a short-term liquidity buffer, and document guardrails that trigger spending reviews. Periodic plan checks—annually or when portfolio value moves by a material percentage—help translate strategy into practice. Combining dynamic methods with the 4% benchmark, sequence risk mitigation tactics, and the other concepts explored in this content package builds a coherent approach that adapts to changing conditions.

Related Articles

- How Much Can You Safely Withdraw in Retirement Without Running Out of Money? Practical Strategies for U.S. Families

- The 4% Rule: Origins, Strengths, and Limitations

- Sequence of Returns Risk and How Withdrawals Affect Portfolios

- The 401(k) Tax Trap Most Retirees Don’t See Coming — What It Is and How to Respond

- 7 Retirement Risks That Could Derail Your Retirement Plan

- IULs vs Fixed Indexed Annuities for retirement income: How to Compare the Two

About the Author

John P. Sansaricq is a licensed insurance professional focused on retirement income planning, life insurance strategies, and educational resources for pre-retirees and retirees.

He helps individuals and families explore ways to protect savings, manage risk, and prepare for more informed retirement planning conversations.

Plan Your Retirement Income With Confidence

If this topic raised questions about retirement income, taxes, market risk, or long-term planning, the next step is to review a simple educational guide and prepare for a strategy conversation.

Download the free guide: Safe Withdrawal Strategies: How Much You Can Withdraw in Retirement Without Running Out of Money