In This Series

In This Guide

Key Takeaways

- Sequence of returns risk can sharply reduce portfolio longevity if early retirement years coincide with market weakness

- Holding a short-term cash reserve or laddered fixed income can prevent forced portfolio withdrawals during downturns

- Withdrawal rules that adapt to portfolio performance reduce the probability of depleting assets

Angle: A focused analysis of sequence of returns risk with actionable tactics such as cash reserves, bond ladders, and withdrawal smoothing that help mitigate early-retirement market shocks.

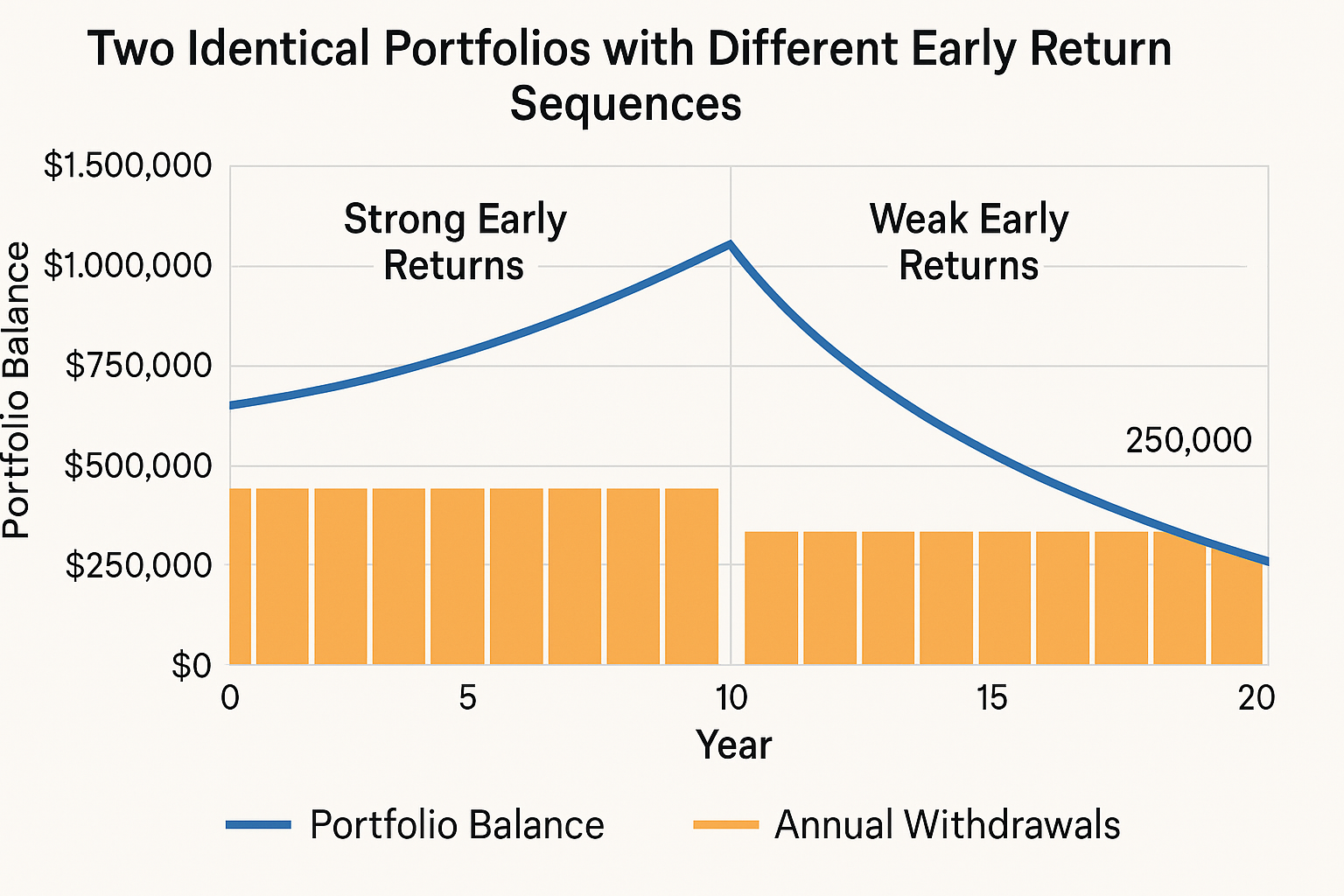

How Sequence of Returns Changes Outcomes

Two retirees with identical portfolios and the same average long-term return can face vastly different outcomes if returns occur in a different order. Withdrawals during a market downturn lock in losses by reducing the asset base that later returns would compound. As a result, timing matters: negative returns in the early retirement years produce larger effects on longevity than the same returns later. Understanding this mechanism is central to choosing a withdrawal approach that protects against early shocks.

Practical Tactics to Cushion Early Years

Maintaining a cash reserve of one to three years of spending reduces the need to sell growth assets during a downturn, which can preserve long-term portfolio health. A bond ladder that matures in successive years serves a similar purpose, offering predictable cash flow without market exposure. Additionally, temporary spending adjustments and discretionary spending flexibility during market stress can materially extend portfolio life without permanently changing retirement lifestyle.

Withdrawal Smoothing and Adaptive Rules

Withdrawal smoothing techniques lower the probability of ruin by tying annual withdrawals to recent portfolio performance or by using a percentage-of-portfolio rule that naturally declines when the portfolio shrinks. Spending bands establish upper and lower limits and trigger modest adjustments only when portfolio value moves outside those bands. These adaptive methods balance the desire for spending stability with the practical need to respond to market realities, and they work well in conjunction with contingency reserves and income sources.

Related Articles

- How Much Can You Safely Withdraw in Retirement Without Running Out of Money? Practical Strategies for U.S. Families

- The 4% Rule: Origins, Strengths, and Limitations

- Adjusting Withdrawals: Dynamic Methods and Budgeting Tools

- IULs vs Fixed Indexed Annuities for retirement income: How to Compare the Two

- 401k Retirement Income Strategy: How to Turn Savings Into a Reliable Paycheck

- When Should You Take Social Security? (62 vs 67 vs 70) — How to Compare Your Options

About the Author

John P. Sansaricq is a licensed insurance professional focused on retirement income planning, life insurance strategies, and educational resources for pre-retirees and retirees.

He helps individuals and families explore ways to protect savings, manage risk, and prepare for more informed retirement planning conversations.

Plan Your Retirement Income With Confidence

If this topic raised questions about retirement income, taxes, market risk, or long-term planning, the next step is to review a simple educational guide and prepare for a strategy conversation.

Download the free guide: Safe Withdrawal Strategies: How Much You Can Withdraw in Retirement Without Running Out of Money