In This Series

In This Guide

Key Takeaways

- Safe withdrawal rates are not one-size-fits-all; they depend on lifespan, portfolio mix, and other income sources

- The traditional 4% rule offers a baseline but may be less reliable under low-return or high-inflation conditions

- Flexible withdrawal strategies and contingency reserves help manage sequence-of-returns risk

- Regular plan reviews and scenario testing support long-term sustainability

Understanding the Basics of Withdrawal Sustainability

Sustainable withdrawal strategies aim to provide income today while maintaining enough assets to support future spending needs. A key metric is the initial withdrawal rate, typically expressed as a percentage of the total retirement portfolio. That number interacts with portfolio return assumptions, inflation, and the expected retirement horizon. For U.S. families, predictable income sources such as Social Security or pensions reduce dependence on portfolio withdrawals, while required minimum distributions and taxes can change net cash flow needs. Thinking about withdrawals in terms of scenarios—best case, expected, and worst case—helps translate a percent into realistic spending plans.

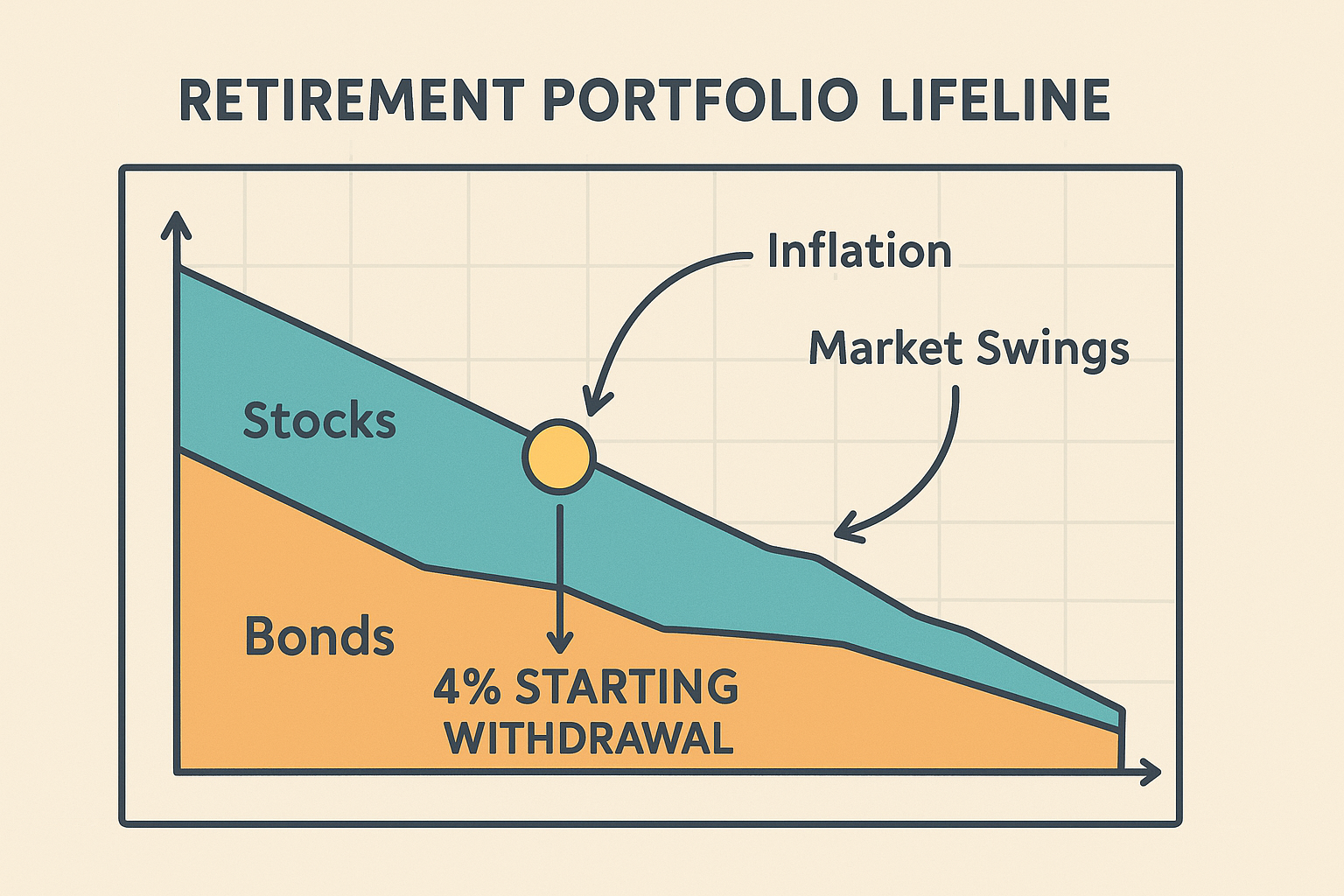

The 4% Rule: Why It Matters and Where It Falls Short

The 4% rule became popular because it distilled decades of market data into a single, easy-to-use starting point: withdraw 4% of your portfolio in year one and adjust that dollar amount for inflation each subsequent year. It offers simplicity and a historical track record for a diversified portfolio over a 30-year horizon. However, modern research and recent market conditions show the rule can be sensitive to low long-term returns, high inflation, and unlucky early-year market declines. For readers interested in a deeper dive, the supporting article The 4% Rule: Origins, Strengths, and Limitations examines historical simulations, common misconceptions, and scenarios where alternative approaches may be preferable.

Strategies to Reduce the Risk of Running Out of Money

Several practical strategies can lower the chance of depleting assets. Maintaining a short-term cash reserve or a bond ladder smooths withdrawals during market downturns. Dynamic withdrawal rules, such as percentage-of-portfolio withdrawals or spending bands that shrink or expand with portfolio performance, align spending to actual portfolio value. Partial annuitization and delaying Social Security are other ways families can increase reliable lifetime income, though those choices carry different trade-offs and timelines. Sequence of returns risk deserves particular attention because poor returns in the first few retirement years can have outsized effects; the supporting article Sequence of Returns Risk and How Withdrawals Affect Portfolios explores this in more detail.

A Practical Framework to Decide How Much to Withdraw

Begin by estimating baseline spending needs and identifying fixed income sources. Next, decide on a starting withdrawal approach—many households use a conservative starting percentage or a percentage-of-portfolio rule that adjusts with market value. Build in a contingency reserve to cover 1–3 years of spending and set guardrails that trigger spending adjustments if portfolio value falls below thresholds. Regularly revisit assumptions and run scenario tests under different return and inflation outcomes. For hands-on techniques such as withdrawal smoothing and budget-linked spending adjustments, consult the supporting article Adjusting Withdrawals: Dynamic Methods and Budgeting Tools.

Frequently Asked Questions

What constitutes a safe withdrawal rate in retirement?

A safe withdrawal rate balances current spending needs with the goal of preserving assets for future years. It depends on lifespan expectations, portfolio allocation, other income sources, and tolerance for market volatility. Using historical benchmarks such as the 4% rule can help frame initial planning, but many households adopt flexible methods and contingency reserves to adapt to changing returns and inflation.

Is the 4% rule still a good starting point?

The 4% rule remains a useful starting benchmark for many retirees because of its simplicity and historical basis, but it is not universally right. Low expected returns, high inflation, long retirement horizons, and sequence of returns risk can make a fixed 4% approach less appropriate. Combining the 4% benchmark with adaptive withdrawal rules and reserves often yields a more resilient plan.

How does inflation affect safe withdrawals?

Inflation erodes purchasing power and increases the dollar amount needed to maintain a given lifestyle, which makes inflation-linked adjustments an important consideration. Fixed-dollar withdrawals that are not adjusted for inflation lose real value over time, while aggressive inflation adjustments during prolonged high inflation can raise the risk of depleting assets. Budgeting, flexible spending rules, and income sources pegged to inflation help manage this challenge.

What steps can reduce the risk of running out of money?

Actions that reduce longevity risk include maintaining a short-term liquidity buffer, using adaptive withdrawal rules like spending bands or percentage-of-portfolio methods, diversifying across asset classes, and aligning essential expenses with reliable income sources. Regularly reviewing assumptions, conducting scenario tests, and separating essential from discretionary spending also help maintain a sustainable withdrawal plan.

Related Articles in This Series

- The 4% Rule: Origins, Strengths, and Limitations

- Sequence of Returns Risk and How Withdrawals Affect Portfolios

- Adjusting Withdrawals: Dynamic Methods and Budgeting Tools

- 7 Retirement Risks That Could Derail Your Retirement Plan

- Implementing IUL Strategies for Retirement Income: Design, Risks, and Steps

- The 401(k) Tax Trap Most Retirees Don’t See Coming — What It Is and How to Respond

About the Author

John P. Sansaricq is a licensed insurance professional focused on retirement income planning, life insurance strategies, and educational resources for pre-retirees and retirees.

He helps individuals and families explore ways to protect savings, manage risk, and prepare for more informed retirement planning conversations.

Plan Your Retirement Income With Confidence

If this topic raised questions about retirement income, taxes, market risk, or long-term planning, the next step is to review a simple educational guide and prepare for a strategy conversation.

Download the free guide: Safe Withdrawal Strategies: How Much You Can Withdraw in Retirement Without Running Out of Money